Key takeaways:

- The UAE eWallet market is projected to reach $498.15 million by 2032, growing at a CAGR of 17.63%.

- Building an eWallet app in the UAE typically costs between $30,000 and $150,000, depending on features and compliance scope.

- A CBUAE license (SVF or RPSCS) is mandatory before launch, and mapping the right category early avoids costly delays later.

- Security, KYC/AML compliance, and a smooth onboarding experience are what separate a trusted eWallet app from one users abandon.

The UAE is racing toward a cashless future, with the eWallet development market expected to reach $498.15 million at a CAGR of 17.63% by 2032, according to the Market and Data. Businesses have also started taking action to get a share of this and have started asking the question: how to develop an eWallet app in UAE.

From retail brands to fintech startups, everyone is chasing the solution for this problem, building an eWallet app that is trusted by people and solves their financial transaction headaches. A successful eWallet app is not just a payment button bolted into an app; it is a secure, compliant, and genuinely useful digital payment app that people rely on every day.

In this blog, we will walk through how to build an eWallet app in UAE from scratch, taking care of every fintech development aspect from regulation to features and cost.

Let’s Get Started.

What is an eWallet App?

An eWallet app is a mobile application for storing payment details, funds, and identity credentials securely on your smartphone. Rather than real cards or cash, customers make purchases, move money, and manage their affairs directly using an eWallet app.

Most individuals already use one, whether it is a virtual wallet app issued by a bank or a stand-alone digital payment platform used for online shopping and bill payments. An eWallet does three things well fundamentally: it securely holds value or payment credentials, it verifies the user’s identification, and it processes transactions swiftly.

Understanding this foundation matters before any digital wallet development work begins.

Why the UAE & GCC Are Prime Ground to Build an eWallet App?

The UAE is one of the fastest-moving cashless economies in the world. Government-backed digital payment initiatives, near-universal smartphone usage, and a tech-savvy, primarily expat populace have created perfect conditions for any cashless payment software to prosper. Surveys have revealed that the majority of UAE inhabitants foresee a completely cashless country in the next few years, and consumer behavior is already going in this direction, with in-store card and mobile payments constantly outpacing cash.

This demand has resulted in fierce competition among ewallet app development companies in Dubai, all trying to service retail, logistics, telecom, and travel brands who are looking for their own branded mobile payment solution. Dubai and Abu Dhabi are still the commercial centers, but the opportunity is not exclusive to the UAE.

Demand is also rising quickly further out across the Gulf. An eWallet startup in Oman, for instance, may capitalize on similar smartphone-first, underbanked-to-banked demographic changes, while Saudi Arabia and Bahrain are working their own national digital payment agendas. The UAE provides a powerful domestic market and a launchpad to the whole GCC area for any business that chooses to develop an eWallet software today.

Industry Insight

According to the Central Bank of UAE (CBUAE), the National Payment Systems Strategy (NPSS) aims to make the UAE a leading cashless economy by enabling secure, innovative, and convenient electronic payments while connecting banks, exchange houses, and eWallets in a unified payment ecosystem.

UAE Regulatory Landscape You Must Understand First

Anyone planning to build an e-wallet software in the UAE has to understand who governs it and how, before creating a single line of code. Unlike many marketplaces, payment activity in mainland UAE is directly overseen by the Central Bank of UAE (CBUAE). Not doing this is the quickest way to construct something that you can’t lawfully launch.

Stored Value Facilities (SVF) Regulation

This framework applies if your app retains client balances, sometimes referred to as a “float.” It requires a minimum of $4.1 million paid-up capital, an Aggregate Capital Fund of at least 5% of the float, and stringent regulations on the protection of customer funds, including daily reconciliation and retention of data for five years.

Retail Payment Services and Card Schemes (RPSCS)

The rule also covers wider payment activities, such as the issuing of payment accounts, merchant acquiring and cross-border transfers. It is split into license categories with capital needs from about $27,000 to $820,000 depending on the range of services offered.

Crypto Wallets and VARA

If your product is involved with bitcoin or virtual assets, then you will be dealing with a distinct authority, the Virtual Assets Regulatory Authority (VARA). Because the regulatory perimeters are completely different, crypto activity is often kept in a separate legal organization from currency wallet operations.

Free Zone Rules: DIFC and ADGM

Financial free zones such as DIFC and ADGM have their own independent regulators (DFSA and FSRA, respectively) and licensing procedures separate from mainland UAE. A business registered in DIFC cannot just act as a mainland payment provider without further permissions and vice versa.

This is not legal advice, and the rules change; thus, any serious eWallet app development plan should engage compliance counsel early, not after the app is launched. That’s what the regulatory backbone tells you quite plainly: that a fintech wallet software in the UAE is examined for its compliance architecture as much as for its functionality. This is the component that distinguishes a genuine fintech app development solution from an app that gets stuck at the licensing stage from day one.

Answer a few quick questions and our experts will share a tailored project estimate.

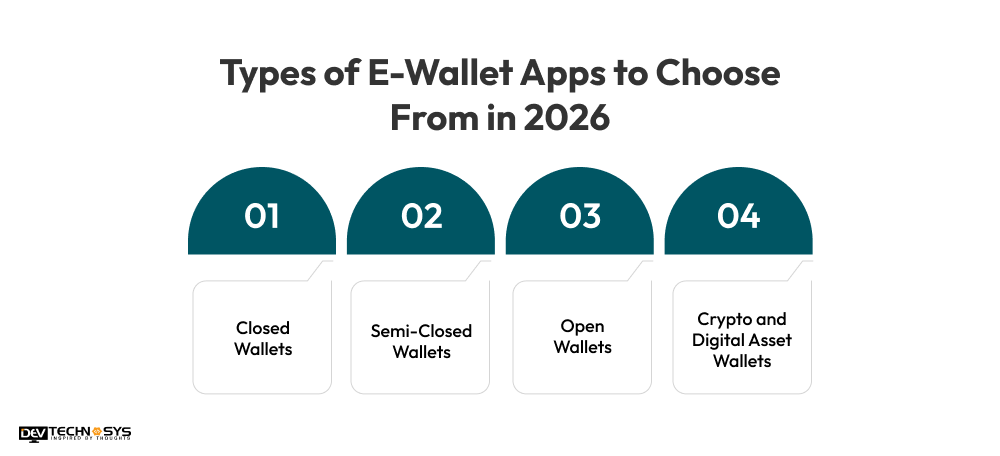

Types of E-Wallet Apps to Choose From in 2026

Not all e-wallets are the same, and the decisions you make early on about the type of e-wallet you want to build will impact everything from your licensing process to your technology stack. Wallet app development can be classified broadly into 4 types.

Closed Wallets

These are limited to a specific platform, such as a retailer’s in-app credit that may only be used for that brand’s products. They are easiest to develop and often have the least regulatory load; thus, they are a typical starting point for a bespoke eWallet app.

Semi-Closed Wallets

These allow you to spend at a network of linked merchants rather than a single brand. A good regional example is a business that chooses to build an app like Touch n Go, which enables customers to pay across transport, retail and services inside a connected merchant environment, without complete open-loop banking access.

Open Wallets

These are the most powerful and most regulated, because they connect directly to bank accounts and card networks, and allow withdrawals, transfers and broad merchant acceptance. In the UAE, businesses that want to develop an app like Payit are essentially targeting this segment, which is a full-fledged, bank-grade payment wallet app that can be used for anything from bill payments to P2P transfers.

Crypto and Digital Asset Wallets

They deal in and hold cryptocurrencies or tokenized assets, not fiat currency, and are regulated by VARA rather than by the CBUAE’s standard payment structures.

Each type requires a different architecture for the smart wallet software; therefore, this decision must be made before any design or development work begins, not after.

Industry Stat

According to Visa’s Stay Secure Study, 81% of UAE consumers expect to use digital payments more frequently over the next 12 months, highlighting the country’s growing preference for cashless transactions.

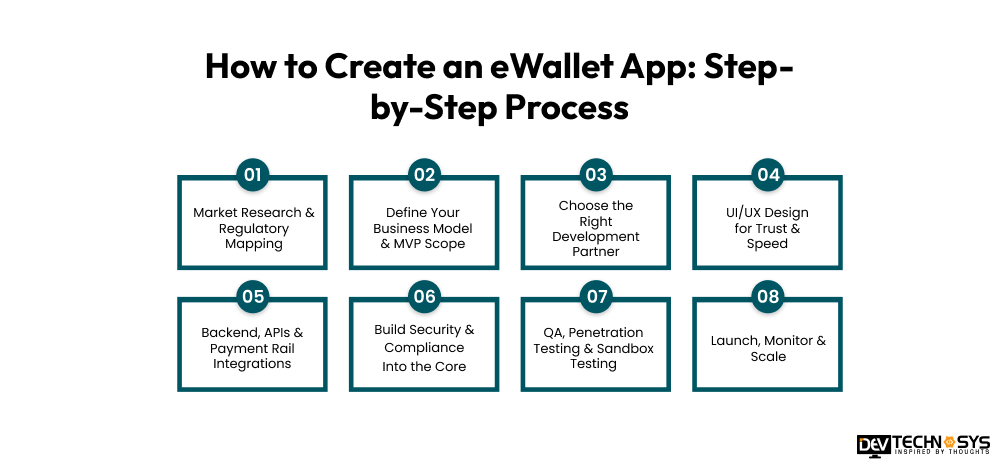

How to Create an eWallet App: Step-by-Step Process

Once you know your wallet type and regulatory path, the actual build follows a clear sequence. Skipping steps here is where most projects run into delays.

Step 1: Market Research & Regulatory Mapping

First, define your target users, your rivals, and the CBUAE licensing category to which your wallet type belongs. You want to do this mapping before you do any design work, because it defines your capital requirements, your timeframe, and even what features you’re legally allowed to ship at launch. Some businesses choose to develop ewallet apps without this stage, only to find license holes halfway through development, which is much more expensive to correct later.

Step 2: Define Your Business Model & MVP Scope

Choose a revenue plan for your wallet: transaction fees, subscriptions, float interest, or B2B licensing to other firms. Rather than trying to launch all your features at once, cut your first release down to a true MVP with core payments, onboarding, and a couple of killer features.

Step 3: Choose the Right Development Partner

Your development partner should have an established fintech portfolio, direct experience with UAE compliance regulations, and security certificates to back it up. Many owners prefer to hire dedicated developer teams to construct the in-house team from scratch, as it helps to decrease the hiring process and gives quick access to specialists who already know payment architecture.

Step 4: UI/UX Design for Trust & Speed

Getting wallet onboarding to seem fast and trustworthy is no mean feat, yet it’s what’s needed. You should give priority to biometric login, minimum form fields, and keep transaction confirmation very clear. UAE has a diverse linguistic user base, so you should prefer billing in both Arabic and English layouts simultaneously from day one.

Step 5: Backend, APIs & Payment Rail Integrations

This is where the wallet does the actual money moving. Here the backbone is a strong ledger system, tokenization for saved card data, and a clear API integration with banks and payment gateways. In UAE, you should look to hook up to local payment rails as well as regular card networks, and establish reliable peer-to-peer (P2P) transfers so users can send money to each other instantaneously, not only to businesses.

Step 6: Build Security & Compliance Into the Core

Security is essential and should be integrated even before you launch; it should not be built after launch. From day one, you should integrate features such as encryption, multi-factor authentication, device binding, and real-time fraud detection with KYC and AML workflows to meet license-category demands.

Step 7: QA, Penetration Testing & Sandbox Testing

Before launching, it is essential to undergo QA, third-party penetration testing, and regulatory sandbox testing to keep high-quality standards even before the game starts. This helps uncover vulnerabilities and compliance gaps without losing extra budget, as they will be affordable as of now without real cash online.

Step 8: Launch, Monitor & Scale

Launch should be a phased rollout with careful monitoring of trends in initial weeks, dedicated support, and keeping a specific compliance team in place. It is also essential to plan support services from the start, as mobile app maintenance costs are recurrent and not a one-time purchase; these include bug corrections, security patches, and feature updates as your user base grows.

Must-Have Features To Develop an eWallet App in 2026

The features of an eWallet app decide whether users open it once and abandon it, or make it part of their daily routine. Getting the essentials right matters more than chasing every trend at once.

Essential Features

- Onboarding and KYC verification: The app should incorporate Emirates ID-based identity checks for new users, in conformity with the regulations in the UAE.

- Multiple payment options: Users should be able to pay by card, bank transfer, or contactless payment via NFC and not be confined to one way only.

- Peer-to-peer (P2P) transfers: Users want to immediately send and receive money, not just pay businesses.

- Bill payments: Direct connectivity with utility and telecom companies including DEWA, du and Etisalat means users may pay recurring bills without leaving the app.

- Transaction history and real-time alerts: Every payment should be transparently tracked with fast alerts so users always know where their money is going.

- Biometric login: Quick access with Face ID or fingerprint authentication, keeping your account secure.

- In-app customer support: Live chat or help center allows consumers to fix payment concerns without leaving the app.

Advanced and Differentiating Features

- Support for many currencies: This is particularly helpful in the UAE, which has a big population of expats, many of whom transmit money across borders on a daily basis.

- QR code payments: Quick and contactless transactions in stores or between users.

- Cashback and loyalty rewards: These help keep customers engaged with the app even after their first transaction.

- In-app bill splitting: This feature makes it easy to split costs with friends or roommates.

- Budgeting and spend tracking features: Turning the wallet into more than a digital payment software, these capabilities provide customers the ability to manage their money directly.

- Merchant dashboard integration: Businesses can use this to turn their wallet into a point-of-sale tool.

- Voice-Enabled Payments: A rising convenience option for users wanting to transact hands-free.

- Dark mode and accessibility options: These little things make the daily use more pleasant for a broader spectrum of users

Latest Tech Stack for eWallet App Development

Your choice of tech stack depends on your wallet type and target platforms, but most of the UAE eWallet initiatives tend to converge around a similar set of proven technologies. Native Android app development or cross-platform? This typically depends on your budget, timeline, and how much the app needs to access device-level security features.

Layer |

Common Technologies |

Why It Matters |

| Frontend (Mobile) | Kotlin (Android), Swift (iOS), Flutter, React Native | Determines app speed, native feel, and biometric integration depth |

| Backend | Node.js, Java, .NET | Handles transaction logic, ledger management, and API Integration |

| Database | PostgreSQL, MongoDB | Stores user data and transaction records with strict consistency guarantees |

| Cloud Infrastructure | AWS, Microsoft Azure | Provides scalability and, critically, UAE-based data residency options |

| Security Layer | AES-256 encryption, tokenization, MFA | Protects stored data and meets CBUAE and PCI DSS requirements |

| Payment Integration | Payment gateway SDKs, card network APIs | Connects the wallet to banks, card schemes, and local payment rails |

Businesses are often in a dilemma of native development vs a single codebase from a hybrid app development company, since a shared codebase can save them a lot in terms of cost and time to market without compromising much on performance.

What is the Cost to Build an eWallet App in the UAE?

The cost to create an eWallet app in UAE varies widely depending on complexity, depth of features, and compliance requirements. But most projects fall into a predictable range. A simple wallet with fundamental payment functions is much less expensive than a fully licensed, bank-grade platform developed to scale. The common benchmark for ewallet app development cost is between $30,000 and $150,000, but enterprise-grade implementations with custom integrations and enhanced compliance might be more than that.

Tier |

Estimated Cost (USD) |

What’s Included |

| Basic | $30,000 – $60,000 | Core wallet features, single payment gateway, basic KYC, simple UI |

| Mid-Level | $60,000 – $100,000 | Multiple payment integrations, biometric login, P2P transfers, advanced KYC/AML workflows |

| Advanced | $100,000 – $150,000+ | Full CBUAE compliance architecture, multi-currency support, fraud detection, custom backend, merchant dashboard |

Factors that affect the cost to make an eWallet app:

The table below breaks down what actually drives the price up or down within each tier.

Regulatory & Compliance Scope

There’s a lot of backend and legal work to get the CBUAE licensing requirements, KYC/AML protocols, and data residency rules in place. This is frequently the biggest expense factor for any major wallet project, since compliance cannot be an afterthought that is slapped on before launch.

Feature Complexity

Basic payments cost less than complex services like P2P payments, multi-currency support, or merchant dashboards. Every added feature requires time for creation, testing, and maintenance, and this quickly adds up across a full feature set.

Platform Choice

Separate Android and iOS development is more expensive than a single codebase for both platforms. Native apps can provide faster performance and more in-depth device integration, but that comes at a higher cost and longer timeline.

Third-Party Integrations

Every payment gateway, bank API, or card network link needs to be integrated and tested. Costs grow further if specialized middleware is required to interface systems that weren’t originally designed to work together natively.

Security Architecture

Encryption, fraud detection, and penetration testing all demand specialist skills. The cost of cutting corners here is much higher post-launch, in terms of remediation expenditures and loss of customer trust.

Development Team Location

Rates vary considerably from region to region and are generally benchmarked against general mobile app development costs when firms are planning for a project. Having offshore teams can cut costs, but experience and knowledge of compliance issues are more important here than with ordinary software development.

Industry Insight

According to the UAE’s Telecommunications and Digital Government Regulatory Authority (TDRA), UAE PASS has facilitated over 2.6 billion digital transactions across government and private-sector services, reflecting the country’s mature digital infrastructure.

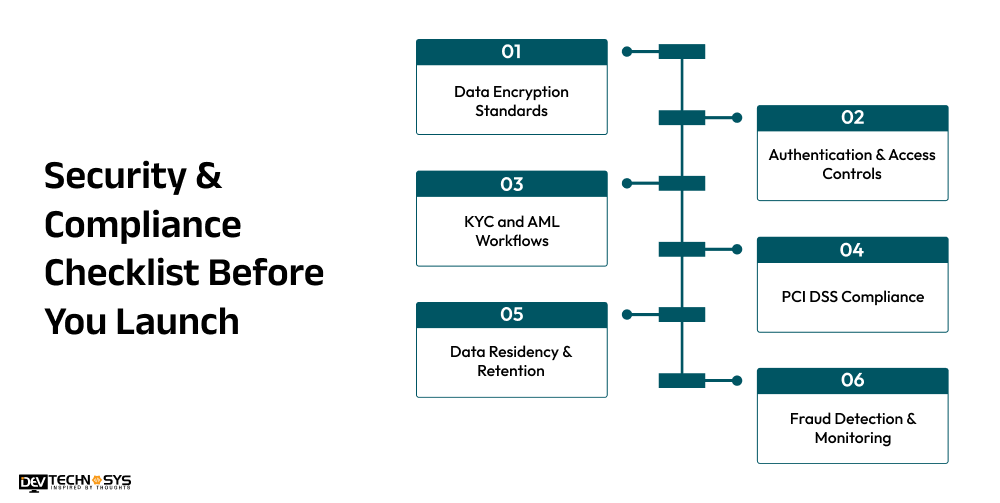

Security & Compliance Checklist Before You Launch

Security and compliance can’t be an afterthought. Those need to be proactively checked out before launch, not found as holes once real customer money is on the line.

Data Encryption Standards

Ensure that all data saved and transferred is protected with strong encryption, often AES-256 for data at rest and TLS for data in transit. Any hole here is one of the fastest ways to fail a security audit.

Authentication & Access Controls

Biometric login, multi-factor authentication, and device binding should all be live at launch, not added later as an upgrade. These layers are what protect against unwanted access even if a password is compromised.

KYC and AML Workflows

Identity verification and anti-money laundering checks must be strictly in compliance with the exact category of your CBUAE license. One of the most frequent causes for wallet launches to be delayed at the regulatory review stage is under-scoping.

PCI DSS Compliance

If the wallet in any way processes card data, PCI DSS compliance is not optional. This includes safe card tokenization and rigorous rules about how cardholder data is stored, handled, and sent.

Data Residency & Retention

Check where user data is physically located and how long it is retained. In the UAE, legislation usually stipulates local data residency and minimum retention durations, and this needs to be architected in from day one, not patched.

Fraud Detection & Monitoring

Transaction monitoring and fraud scoring should be real-time from day one, and there should be explicit escalation processes for detected transactions before they get to the end user.

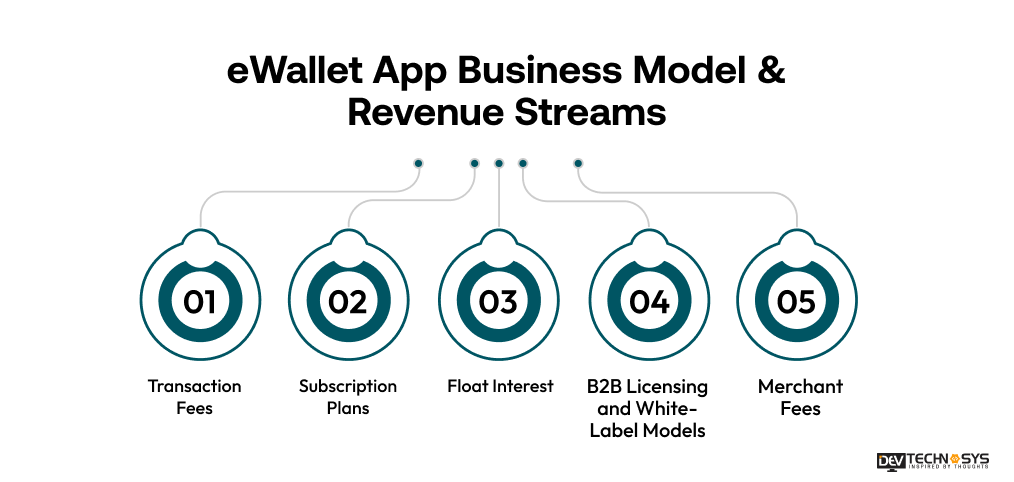

eWallet App Business Model & Revenue Streams

Before development starts, it helps to be clear on how the wallet will actually make money. The right eWallet app business model shapes everything from feature priorities to which user segment you target first.

Transaction Fees

The most common model charges a small percentage or flat fee per transaction, whether that’s a merchant payment, a P2P transfer, or a cross-border remittance. This works well for high-volume digital payment platforms but requires enough transaction flow to be sustainable.

Subscription Plans

Some wallets charge users or businesses a recurring fee for premium features, like higher transfer limits, priority support, or advanced budgeting tools. This model suits wallets targeting power users rather than casual, occasional spenders.

Float Interest

Wallets holding customer balances can earn interest on that float, subject to CBUAE safeguarding rules. This is a slower-building revenue stream but adds up meaningfully at scale.

B2B Licensing and White-Label Models

Rather than building a consumer brand from scratch, some companies license their wallet infrastructure to other businesses, an approach commonly built through hybrid app development services that let a single core platform power multiple branded frontends.

Merchant Fees

Charging merchants a fee to accept payments through the wallet, similar to card network models, is another reliable stream, particularly once a wallet reaches meaningful merchant adoption. Most successful wallets combine two or three of these models rather than relying on just one.

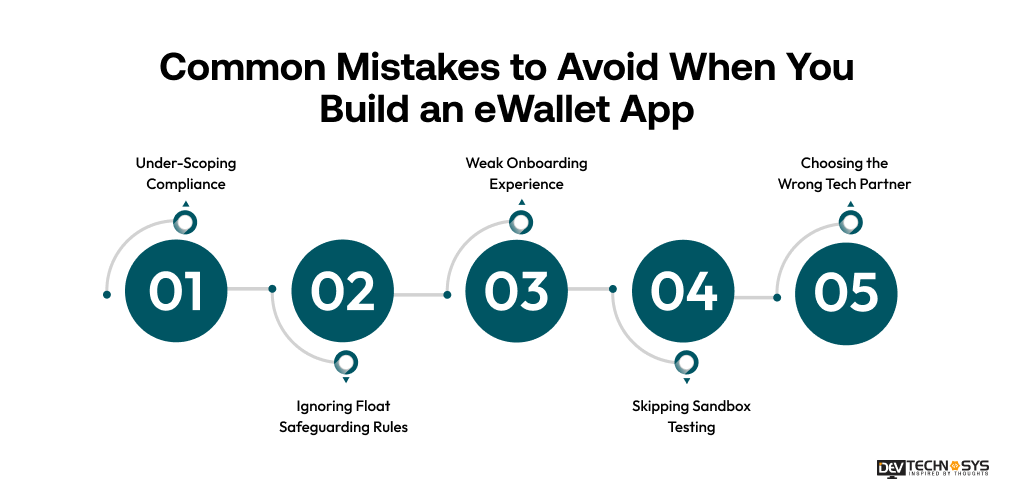

Common Mistakes to Avoid When You Build an eWallet App

Even well-funded projects run into avoidable problems. Knowing these in advance can save months of rework.

Under-Scoping Compliance

Many teams treat regulatory requirements as a checklist to complete near launch, rather than a foundation to design around from day one. This almost always leads to costly rebuilds once the actual license category and its requirements become clear.

Ignoring Float Safeguarding Rules

If your wallet holds customer balances, safeguarding requirements around reconciliation and fund segregation need to be built into the architecture early, not patched in after an audit flags the gap.

Weak Onboarding Experience

A confusing or lengthy sign-up process is one of the biggest reasons users abandon a mobile wallet app before ever making their first transaction, no matter how strong the backend is.

Skipping Sandbox Testing

Launching without proper sandbox and penetration testing means real users become the test group, which is a risky and expensive way to discover security gaps.

Choosing the Wrong Tech Partner

Selecting a team based on cost alone, without verifying real fintech experience, often costs more in the long run through delays and rework.

Conclusion

To develop an e-wallet app in UAE is a genuine regulatory challenge; the market opportunity more than makes up for the effort. From understanding CBUAE licensing types to developing the correct security architecture to picking a business model that fits your consumers, every step in this tutorial plays a factor in whether the wallet will win true trust and regular use.

The businesses that nail this are the ones that approach compliance, security, and user experience as equally critical from day one, not as an afterthought. No matter if you are establishing a closed loyalty wallet or want to go all the way with a complete open wallet with bank-grade capabilities, collaborating with the proper ewallet app development company makes all the difference in getting there smoothly.

FAQs

Q1. How Much Does It Cost to Develop an eWallet App in UAE?

The cost to create an eWallet app generally ranges from $30,000 to $150,000 based on features, compliance scope, and platform choice. Basic wallets are on the low end, and comprehensive designs with full CBUAE compliance, multi-currency compatibility, and fraud detection are on the high end, driving costs higher.

Q2. Do I Need a License From the Central Bank of UAE to Launch an eWallet?

Yes, mostly. Customer balance wallets need an SVF license, and other payment services are covered by RPSCS. Which category exactly relies on what your pocketbook can do. Mapping this out early saves you pricey delays in the road.

Q3. How Long Does It Take to Build an eWallet App?

Most e-wallet projects take four to nine months depending on the complexity of features and compliance requirements. Simple MVP wallets can go to market faster, and fully compliant, bank-grade wallets with various connectors tend to be closer to the longer end of that spectrum.

Q4. What is the Difference Between a Closed, Semi-closed, and Open eWallet?

Closed wallets work only within one brand. Semi-closed wallets work across a network of affiliated merchants. Open wallets connect directly to bank accounts and card networks, allowing withdrawals and broad merchant acceptance, making them the most regulated of the three.

Q5. Can a Startup Launch an eWallet App in a UAE Free Zone?

Yes. Free zones like DIFC and ADGM operate under their own regulators, DFSA and FSRA, with separate licensing paths from mainland UAE. Startups often choose this route for faster setup, though it comes with its own compliance requirements.

Q6. What Security Standards Does an eWallet App Need to Meet?

At minimum, AES-256 encryption, multi-factor authentication, and PCI DSS compliance for card data. UAE wallets also need robust KYC and AML workflows, real-time fraud detection, and clear data residency practices to meet CBUAE expectations.

Q7. Can I Add Cryptocurrency Support to My Digital Wallet App?

Yes, but it falls under a different regulator, VARA, rather than the CBUAE. Most businesses keep crypto and fiat wallet operations in separate legal entities to stay compliant with both regulatory frameworks cleanly.

Q8. Should I Build an eWallet App in-house or Hire a Development Agency?

Hiring an experienced agency is usually faster and lower-risk, since fintech-specific compliance and security expertise takes years to build in-house. In-house teams make sense mainly for large companies planning multiple long-term financial products.

{kind=link}