Key Takeaways:

-

- Entrepreneurs can tap into the rapidly expanding UAE and MENA digital payments market by choosing to build a fintech app like Ziina with a reliable, experienced development partner.

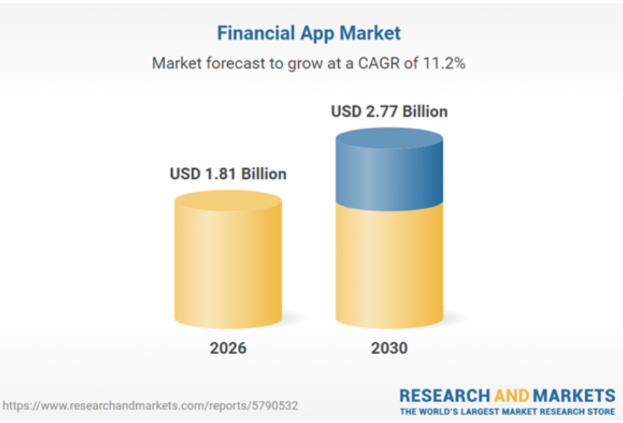

- The global financial app market is projected to grow from $1.63 billion in 2025 to $2.77 billion by 2030 at a CAGR of 11.2%, reflecting enormous untapped opportunity.

- A Ziina clone app delivers instant P2P transfers, biometric authentication, AI-powered fraud detection, multi-currency support, and QR payments, creating a seamless experience that retains users consistently.

- The cost to develop a fintech app like Ziina ranges from $8,000 to $26,000, depending on complexity, features, platform choice, and your chosen engagement model.

Digital payments are no longer a luxury; they are a necessity. Across the Middle East and North Africa, millions of users are ditching cash for smarter, faster alternatives. The UAE, in particular, has emerged as a thriving hub for financial technology innovation.

Ziina stands at the forefront of this revolution. It is a sleek, user-friendly P2P payment platform built specifically for the UAE market. Its rapid adoption proves one thing clearly: consumers want simplicity, speed, and security in one app.

Entrepreneurs and businesses worldwide are taking notice. Many are now exploring how to build a fintech app like Ziina that captures the same seamless experience. Whether you are a startup founder or an established enterprise, this guide covers everything from core features and tech stack to development cost and monetization strategies.

What is Ziina?

Ziina is a licensed, peer-to-peer payment application headquartered in Dubai, UAE. Founded in 2020 by Faisal and Sara Toukan, it simplifies money transfers between individuals using just a phone number or payment link. The platform operates under the UAE Central Bank’s regulatory framework, ensuring complete financial compliance.

Unlike traditional banking apps, Ziina delivers an effortless, borderless payment experience. It eliminates unnecessary friction, no IBANs, no complicated forms. Users simply sign up, verify identity, and begin transacting instantly. As the best fintech app in UAE, Ziina has redefined how residents send, request, and manage everyday payments digitally.

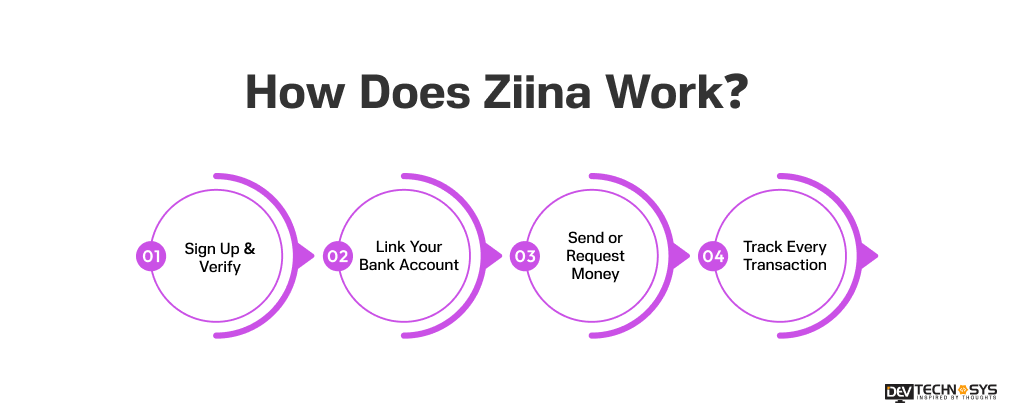

How Does Ziina Work?

Ziina’s simplicity is its greatest strength. The app follows a clean, intuitive flow that anyone can navigate effortlessly.

1. Sign Up & Verify

Users download the app, register with a UAE phone number, and complete a quick KYC verification process within minutes.

2. Link Your Bank Account

Once verified, users securely connect their local UAE bank account or debit card. The process is straightforward, fast, and fully encrypted.

3. Send or Request Money

Users transfer funds instantly using a phone number, QR code, or shareable payment link. Ziina’s secure fintech app architecture keeps every transaction protected and compliant.

4. Track Every Transaction

A clean dashboard displays real-time history, pending requests, and confirmations. A trusted fintech app development company can help replicate this robust, user-first infrastructure effectively.

Markets Stats For Fintech App Development in 2026

The financial app market is expanding at a remarkable pace globally. Here are five critical statistics every entrepreneur must know before entering this space:

- The global financial app market was valued at $1.63 billion in 2025 and is projected to reach $1.81 billion in 2026, growing at a CAGR of 11.4%, driven by rising smartphone penetration and surging digital payment adoption.

- By 2030, the market is expected to hit $2.77 billion at a CAGR of 11.2%, fueled by open banking expansion, real-time transaction monitoring, and personalized finance applications.

- Approximately 63% of SMB workloads were hosted on public clouds by 2023, reflecting how deeply digitalization has penetrated financial services infrastructure worldwide.

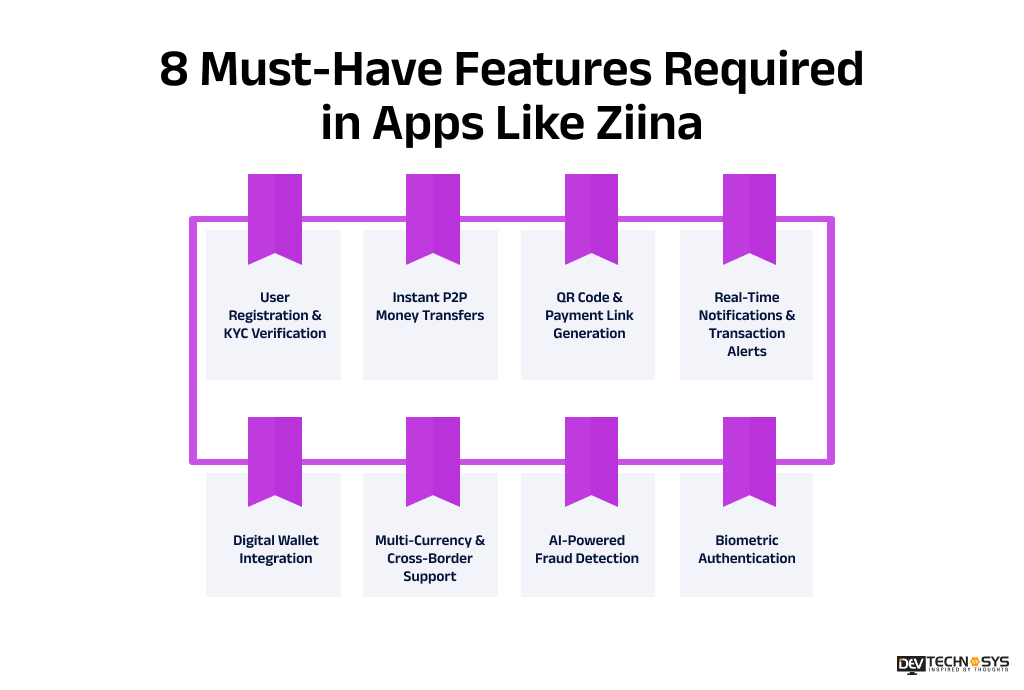

8 Must-Have Features Required in Apps Like Ziina

Building a competitive app like Ziina demands more than just a clean interface. Every feature must solve a real user problem while maintaining ironclad security. Here are eight essential features your app cannot afford to skip.

1. User Registration & KYC Verification

Users onboard quickly through a streamlined sign-up flow. A robust KYC verification system validates government-issued IDs, selfies, and phone numbers, ensuring full regulatory compliance from day one. This is non-negotiable for any banking app development company operating in the UAE market.

2. Instant P2P Money Transfers

The peer-to-peer money transfer feature is the backbone of Ziina’s experience. Users send and receive funds in seconds using just a phone number, QR code, or personalized payment link, no IBAN required.

3. QR Code & Payment Link Generation

Every user gets a unique QR code and shareable payment link. Whether splitting dinner bills or collecting freelance payments, this feature delivers unmatched convenience for daily transactions.

4. Real-Time Notifications & Transaction Alerts

Instant push notifications keep users informed about every debit, credit, and pending request. Real-time alerts dramatically reduce fraud risk and improve overall user trust significantly.

5. Digital Wallet Integration

A built-in digital wallet stores funds securely within the app. This eliminates dependency on external banking apps for every transaction. Seamless ewallet app development ensures users enjoy a unified, frictionless financial experience.

6. Multi-Currency & Cross-Border Support

Supporting multiple currencies positions your Ziina clone app for regional scalability. Users across GCC countries can transact seamlessly without worrying about conversion complications or hidden charges.

7. AI-Powered Fraud Detection

Advanced machine learning algorithms monitor transaction patterns continuously. Suspicious activities trigger immediate flags, protecting users proactively. This capability is indispensable for any PCI DSS-compliant payment app operating at scale.

8. Biometric Authentication

Fingerprint and facial recognition add a powerful security layer. Users authenticate transactions effortlessly without memorizing lengthy passwords, delivering both convenience and enterprise-grade protection simultaneously.

Industry Insights

According to Statista fintech statistics, the global fintech industry has rapidly evolved into a major financial force, with over 3 billion users in digital payments alone by 2024.

Step-by-Step Process to Build a Fintech App Like Ziina

Every successful fintech product begins with a disciplined, well-structured development roadmap. Skipping steps leads to costly reworks and compliance failures. Here is a proven, sequential process to create a fintech app like Ziina from the ground up.

1. Market Research & Competitor Analysis

Understanding your target market is the essential first step. Study Ziina’s user base, pricing model, and regional competitors thoroughly. Identify underserved pain points and untapped opportunities within the UAE and broader GCC payments landscape. Solid research prevents costly assumptions later.

2. Define Your MVP Scope

Avoid building everything at once. A focused MVP development services approach lets you launch faster, gather real user feedback, and iterate intelligently. Prioritize your three to five core features, P2P transfers, wallet, and KYC before expanding further.

3. UI/UX Design

Great fintech apps win users through exceptional design. Invest in intuitive user flows, clean visual hierarchies, and accessible interfaces. Leverage professional front-end development services to craft pixel-perfect screens that feel effortless, because in payments, confusion costs you users permanently.

4. Backend & API Development

A scalable, secure backend is the invisible engine powering everything. Build robust server architecture, implement reliable API integration for payment apps, and connect essential third-party gateways. Your backend must handle high transaction volumes without compromising speed or data integrity under any circumstance.

5. Security & Compliance Implementation

Security cannot be an afterthought; it must be foundational. Integrate end-to-end encryption, multi-factor authentication, and full regulatory compliance protocols from day one. Engaging experienced fintech app development solution providers ensures your architecture meets UAE Central Bank standards without unnecessary delays.

6. Testing & Quality Assurance

Rigorous testing eliminates vulnerabilities before real users encounter them. Conduct functional, performance, penetration, and compliance testing across every module. A single security flaw in a payment app can permanently destroy user trust and attract devastating regulatory scrutiny simultaneously.

7. Launch & Post-Launch Maintenance

A successful launch requires strategic app store optimization, phased rollout planning, and proactive user onboarding. Post-launch, monitor performance metrics continuously. Regular updates, bug fixes, and feature enhancements keep your Ziina app development competitive and users loyally engaged long-term.

Tech Stack for Building a Fintech App Like Ziina

Choosing the right technology stack is the foundation of successful Ziina app development. Every layer must prioritize speed, scalability, and bulletproof security. The table below outlines the precise technologies powering apps like Ziina globally. Selecting battle-tested Android App Development and iOS app development services frameworks ensures your app delivers a native-quality experience across all devices.

| Layer | Technology | Description |

| Frontend | React Native / Flutter | Builds seamless, cross-platform mobile interfaces for both iOS and Android simultaneously |

| Backend | Node.js / Python (Django) | Handles server-side logic, business rules, and high-volume transaction processing efficiently |

| Database | PostgreSQL / MongoDB | Stores transactional data securely with high availability and exceptional query performance |

| API Integration | Stripe, Telr, PayTabs | Enables reliable API integration for payment apps, connecting gateways smoothly for real-time processing |

| Authentication | OAuth 2.0 / JWT / Biometrics | Manages secure login, session handling, and multi-factor user verification effortlessly |

| Cloud Hosting | AWS / Google Cloud | Delivers scalable, reliable infrastructure supporting millions of concurrent users without interruption |

| Security | SSL/TLS / AES-256 Encryption | Protects sensitive financial data through end-to-end encryption across every transaction layer |

| DevOps | Docker / Kubernetes / CI/CD | Automates deployment pipelines, ensuring consistent, rapid, and error-free application releases |

Why Do Entrepreneurs Invest in Fintech Apps Like Ziina?

The UAE’s financial technology landscape presents extraordinary opportunities for forward-thinking entrepreneurs. Millions across MENA remain underserved by traditional banking creating a massive, largely untapped market. Investors recognize this gap instinctively. Create a fintech app like Ziina and you immediately tap into a region experiencing explosive smartphone penetration, progressive regulatory frameworks, and surging consumer appetite for digital-first financial solutions.

1. A Massively Underserved Market Awaits

Despite rapid modernization, millions across MENA lack access to reliable, affordable banking infrastructure. Digital payment platforms bridge this critical gap effortlessly. Entrepreneurs entering this space early capture enormous, loyal user bases before market saturation occurs — establishing dominant brand positioning that becomes extraordinarily difficult for later competitors to displace.

2. Diversified & Recurring Revenue Streams

Fintech platforms generate revenue through multiple simultaneous channels — transaction fees, premium subscriptions, and merchant partnerships compound profitability remarkably fast. Unlike single-revenue businesses, diversified income streams create financial resilience. Even modest per-transaction fees across millions of daily users accumulate into substantial, consistently growing annual revenue figures.

3. Low Operational Overhead, High Scalability

Traditional banking demands enormous physical infrastructure investment. Fintech apps eliminate this burden entirely. Cloud-native architecture scales effortlessly alongside user growth, without proportional cost increases. This exceptional unit economics model makes digital wallet app development one of the most capital-efficient business ventures available to modern entrepreneurs globally.

4. Progressive Regulatory Environment

The UAE government actively champions fintech innovation through forward-thinking regulatory sandboxes and licensing frameworks. Authorities streamline approvals for compliant platforms dramatically reducing market entry timelines. Collaborating with a seasoned fintech app development solution partner ensures your platform navigates this regulatory landscape confidently, efficiently, and without costly compliance missteps.

How Much Does It Cost to Build a Fintech App Like Ziina?

Understanding the Ziina app development cost is critical before committing resources. Development expenses vary significantly based on complexity, feature depth, and your chosen technology partner. However, one truth remains constant: investing in quality architecture from day one prevents enormously expensive fixes later. The table below outlines realistic fintech app development cost estimates across different complexity tiers:

| App Complexity | Features Included | Dev Technosys Cost |

| Basic MVP | Core transfers, KYC, wallet | $8,000 – $12,000 |

| Mid-Level App | MVP + fraud detection, multi-currency | $12,000 – $18,000 |

| Full-Featured App | All features + AI, admin dashboard | $18,000 – $26,000 |

Below are the 7 key factors that influence the cost to develop a fintech app like Ziina:

1. Number of Features

The volume and sophistication of features directly shape your fintech app development cost. Basic functionality demands minimal engineering effort. However, advanced capabilities like AI fraud detection, biometric authentication, and multi-currency wallets require substantially deeper development investment, multiplying both build time and testing complexity considerably.

| Feature Type | Cost Contribution | Examples |

| Basic Features | $500 – $1,500 | Registration, KYC, wallet, transfers |

| Core Features | $1,500 – $2,500 | QR payments, notifications, transaction history |

| Advanced Features | $2,500 – $4,000 | AI fraud detection, biometrics, multi-currency |

2. Platform (iOS / Android / Both)

Platform selection fundamentally determines development scope and mobile app development cost. Building for a single platform reduces initial investment considerably. However, targeting both iOS and Android simultaneously demands parallel development, additional testing cycles, and deeper QA efforts, directly inflating your overall digital wallet app development budget.

| Platform Choice | Cost Contribution | Impact |

| Single Platform | $500 – $1,000 | Faster build, limited audience reach |

| Cross-Platform | $1,000 – $2,000 | Balanced cost, broader user coverage |

| Native iOS + Android | $2,000 – $3,500 | Premium performance, higher investment |

3. UI/UX Complexity

Interface design profoundly impacts user retention and overall Ziina app development cost. A clean, minimal layout is economical and quick to deliver. Conversely, custom animations, accessibility features, and premium interactive dashboards demand significantly more design hours, elevating costs while simultaneously delivering a far superior user experience.

| Design Level | Cost Contribution | Description |

| Basic UI | $300 – $800 | Standard templates, simple navigation |

| Custom UI/UX | $800 – $1,500 | Branded dashboards, moderate customization |

| Premium UI | $1,500 – $3,000 | Advanced animations, interactive features |

4. Third-Party API Integrations

Integrating external services enriches functionality but meaningfully increases API integration for payment apps expenditure. Simple notification APIs are straightforward and affordable. However, connecting sophisticated payment gateways, KYC verification providers, and currency exchange services requires custom development, making this a significant contributor to the mobile payment app development cost.

| Integration Type | Cost Contribution | Examples |

| Basic APIs | $300 – $800 | SMS, email, push notifications |

| Medium Integrations | $800 – $1,500 | Payment gateways, KYC providers |

| Advanced Integrations | $1,500 – $3,000 | Currency exchange, AI tools, open banking |

5. Security & Compliance (PCI DSS)

Financial applications operate under stringent regulatory scrutiny. Implementing robust encryption, data protection protocols, and full PCI DSS compliance adds considerable development overhead. Cutting corners here is catastrophically risky, with regulatory penalties and security breaches costing exponentially more than proper compliance implementation from day one.

| Security Level | Cost Contribution | Features |

| Basic Security | $300 – $1,000 | SSL, basic encryption, secure login |

| Standard Compliance | $1,000 – $1,500 | PCI DSS, two-factor authentication |

| Advanced Compliance | $1,500 – $3,500 | Full audit trails, penetration testing |

6. Team Location & Expertise

Your development team’s geographical location dramatically influences your overall budget. Agencies in North America and Western Europe command premium rates. Meanwhile, equally skilled hire on-demand app developers from South Asia or Eastern Europe, who deliver exceptional quality at significantly more competitive rates without compromising technical sophistication or delivery standards.

| Team Location | Cost Contribution | Hourly Rate |

| South Asia / Eastern Europe | $1,000 – $1,500 | $20 – $50/hr |

| Southeast Asia | $1,500 – $2,000 | $50 – $80/hr |

| North America / Western Europe | $2,000 – $4,500 | $100 – $200/hr |

7. Post-Launch Maintenance

Launching your app is merely the beginning. Ongoing maintenance covering bug fixes, security patches, OS updates, and performance optimization is a perpetual necessity. Neglecting the cost to maintain an app planning leads to technical debt accumulation, ultimately degrading user experience and hemorrhaging your hard-earned user base steadily.

| Maintenance Level | Cost Contribution | Includes |

| Basic Maintenance | $400 – $1,400 | Bug fixes, minor updates |

| Standard Maintenance | $1,400 – $2,500 | Feature updates, security patches |

| Advanced Maintenance | $2,500 – $4,500 | Full optimization, new integrations |

Industry Insight

According to Analytics Insight fintech app trends 2026, fintech apps are increasingly leveraging AI for fraud detection, automated financial management, and personalized insights, transforming apps into proactive financial systems.

What Are the Top 10 Ziina Alternatives?

Before you make a fintech app like Ziina, studying the competitive landscape is absolutely essential. The table below captures ten powerful Ziina app alternative platforms dominating the digital payments space across MENA and beyond.

| App Name | Region | Key Feature | Platform |

| STC Pay | Saudi Arabia | Super wallet + remittance | iOS & Android |

| Mobily Pay | Saudi Arabia | Telecom-integrated payments | iOS & Android |

| Taptap Send | UAE / Global | Cross-border money transfers | iOS & Android |

| Payit by FAB | UAE | Bank-backed digital wallet | iOS & Android |

| Mashreq Neo | UAE | Digital banking + payments | iOS & Android |

| PayBy | UAE | QR payments + remittance | iOS & Android |

| Beam Wallet | UAE | Loyalty + digital payments | iOS & Android |

| NOW Money | UAE | Payroll + wallet for workers | iOS & Android |

| Fawry | Egypt | Bill payments + e-wallet | iOS & Android |

| OPay | Nigeria / MENA | Super financial app | iOS & Android |

1. STC Pay

STC Pay dominates Saudi Arabia’s fintech landscape with seamless P2P transfers, international remittance, and merchant payments. It serves millions of users across the Kingdom. Building a fintech app like STC Pay demands a robust multi-service architecture and deep regulatory compliance.

2. Mobily Pay

Mobily Pay brilliantly integrates telecom billing with everyday digital payments. Users recharge, transfer, and pay bills within one unified platform. Developing a similar app like Mobily Pay requires deep telecom API integration and a frictionless, carrier-grade user experience.

3. Taptap Send

Taptap Send specializes in affordable, lightning-fast international money transfers across MENA and Africa. Its transparent fee structure attracts millions of migrant workers globally. Entrepreneurs looking to develop an app like Taptap Send must prioritize multi-corridor compliance and competitive exchange rate engines.

4. Payit by FAB

Payit, powered by First Abu Dhabi Bank, delivers a fully regulated digital wallet experience for UAE residents. It supports transfers, bill payments, and merchant transactions effortlessly. Those who want to develop an E-wallet app like Payit need strong banking API partnerships and CBU compliance.

5. Mashreq Neo

Mashreq Neo combines full-service digital banking with intelligent payment capabilities. It targets tech-savvy UAE residents seeking a paperless, branch-free banking experience. Entrepreneurs inspired by an app like Mashreq should invest heavily in open banking infrastructure and AI-driven financial insights.

Monetization Models for a Fintech App Like Ziina

Profitability in fintech isn’t accidental; it’s deliberate. When you develop a fintech app like Ziina, selecting the right revenue model determines long-term sustainability. Here are five battle-tested monetization strategies powering today’s most successful digital payment platforms.

1. Transaction Fees

Charging a small percentage per transaction is the most universally adopted fintech revenue model. Users rarely resist minimal fees when the experience delivers genuine value. Even fractional charges across millions of daily transactions generate remarkably substantial, compounding revenue streams over time.

2. Premium Subscription Tiers

Offering tiered subscription plans unlocks predictable, recurring revenue. Free users access basic features while premium subscribers enjoy higher transfer limits, priority support, and exclusive financial tools. This model rewards loyalty while simultaneously incentivizing meaningful upgrades across your growing user base.

3. Merchant Payment Gateway Fees

Onboarding merchants onto your platform creates a powerful dual-sided revenue stream. Businesses pay setup fees and per-transaction commissions for accepting digital payments. As your merchant network expands, this revenue channel scales effortlessly, making it indispensable for any fintech mobile app development solutions strategy.

4. Cross-Border Transfer Margins

International money transfers carry inherent currency conversion costs. Platforms capture revenue through competitive yet profitable exchange rate margins. With millions of expatriates across the UAE and MENA region, cross-border transfers represent an enormously lucrative, high-volume monetization opportunity for similar apps like Ziina platforms.

5. In-App Financial Products

Embedding financial products, microloans, insurance policies, and investment tools transforms your payment app into a comprehensive financial ecosystem. Users access curated products without leaving the platform. This deeply increases engagement, elevates average revenue per user, and positions your app powerfully within the broader fintech app development landscape.

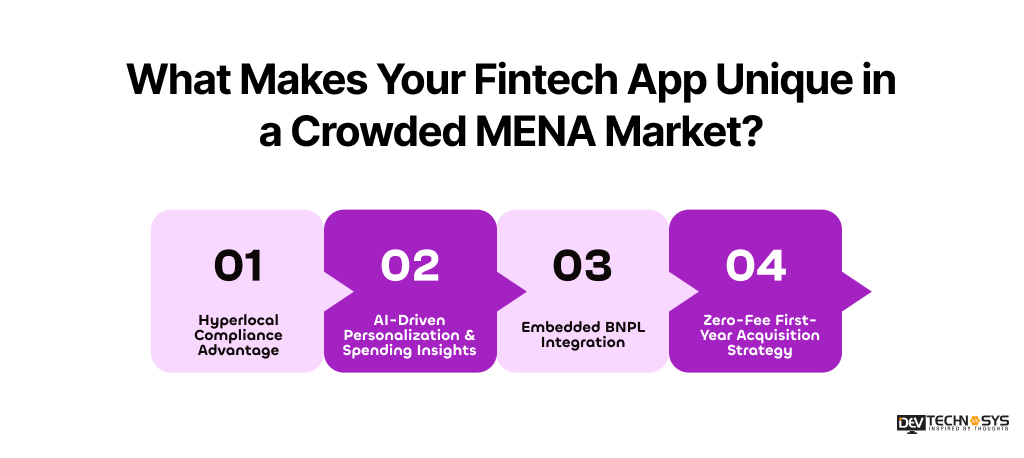

What Makes Your Fintech App Unique in a Crowded MENA Market?

The MENA fintech space is fiercely competitive. Simply replicating features isn’t enough anymore. To build a fintech app like Ziina that genuinely disrupts the market, your platform needs distinctive, defensible advantages that competitors cannot easily replicate overnight.

1. Hyperlocal Compliance Advantage

Embedding UAE Central Bank regulatory compliance and UAE Pass integration from day one creates an insurmountable trust advantage. Users onboard faster, regulators approve quicker, and your platform gains immediate credibility. Most competitors overlook this, making compliance your most powerful, underrated competitive differentiator in the region.

2. AI-Driven Personalization & Spending Insights

Delivering intelligent, personalized spending reports transforms a basic payment app into an indispensable financial companion. Users receive actionable insights tailored to their habits, driving deeper engagement, longer retention, and stronger emotional loyalty toward your platform over generic Ziina app alternative competitors.

3. Embedded BNPL Integration

Integrating Buy Now Pay Later functionality directly within your payment flow unlocks an entirely new revenue dimension. Users split purchases effortlessly without leaving your ecosystem. This frictionless financial flexibility attracts younger, credit-conscious demographics, a massively underserved segment across the e-wallet app like Phonepe landscape.

4. Zero-Fee First-Year Acquisition Strategy

Launching with a bold zero-fee transfer model during your first year aggressively accelerates user acquisition. Early adopters become passionate brand advocates. Once your network effect solidifies, introducing premium tiers feels natural, not forced. This counterintuitive strategy consistently outperforms traditional paid acquisition campaigns across competitive fintech markets.

Conclusion

The UAE’s digital payment revolution is accelerating, and opportunity waits for nobody. Every element covered in this guide features tech stack, cost, and monetization, equipping you with a decisive roadmap to build a fintech app like Ziina confidently.

Success, however, demands the right development partner. With 15+ years of proven expertise, Dev Technosys has delivered hundreds of world-class fintech solutions across global markets. Our battle-tested engineers understand compliance, scalability, and user experience intimately.

Ready to transform your vision into reality? Partner with a trusted fintech software development company and launch your fintech app today.

FAQs

Q1. How Long Does It Take to Develop a Fintech App Like Ziina From Scratch?

The timeline depends heavily on feature complexity and team size. A basic MVP typically takes 1to 2 months. A fully featured platform with AI fraud detection, multi-currency support, and compliance integration requires 3 to 6 months. Proper planning and an experienced development team accelerate delivery significantly without compromising quality.

Q2. Do I Need a Financial License to Launch a P2P Payment App in the UAE?

Absolutely. Operating a P2P payment platform in the UAE mandates licensing from the Central Bank of UAE. The process involves KYC compliance, AML policy documentation, and rigorous security audits. Skipping this step carries severe legal consequences; engaging a compliance consultant from day one is strongly advisable.

Q3. What is the Difference Between a Digital Wallet and a P2P Payment App?

A digital wallet stores funds and payment credentials electronically, functioning like a virtual purse. A P2P payment app specifically facilitates direct money transfers between individuals. Many modern platforms, including Ziina, intelligently combine both functionalities, delivering a unified, comprehensive financial experience within a single, elegantly designed application.

Q4. Can I Build a Ziina-like App That Operates Across Multiple GCC Countries?

Yes, but each GCC country maintains distinct regulatory frameworks. Saudi Arabia, UAE, Kuwait, and Bahrain each require separate licensing and compliance adherence. Building a scalable, multi-corridor architecture from day one ensures smoother regional expansion without costly structural overhauls during later growth phases.

Q5. How Do I Ensure My Fintech App Remains Secure Against Evolving Cyber Threats?

Security requires a proactive, layered approach, not reactive patching. Implement AES-256 encryption, regular penetration testing, and real-time anomaly detection from launch. Conduct quarterly security audits and stay current with PCI DSS standards. Partnering with security-specialized developers ensures your platform evolves defensively alongside increasingly sophisticated cyber threat landscapes.

{kind=link}