Key takeaways:

-

- UAE fintech market size in 2026 is estimated at USD 52.07 billion, with 2031 projections showing USD 90.06 billion.

- The cost to build a fintech app like urpay is estimated between $30,000 to $1,50,000.

- Building a fintech app like urpay requires a structured approach that combines regulatory compliance, secure architecture, and seamless user experience.

- Fintech apps generate revenue through multiple channels by offering payment services, financial products, and premium features

The rise of digital wallets has transformed how people manage money, make payments, and transfer funds. Among the leading fintech platforms in Saudi Arabia, Urpay has gained significant popularity by offering seamless digital payments, international remittances, virtual cards, and secure money management services through a single app.

As cashless transactions continue to grow worldwide, businesses and startups are increasingly exploring opportunities to develop a similar app like urpay. However, fintech mobile app development requires robust security, regulatory compliance, scalable architecture, and innovative features.

This guide explores how to build a fintech app like urpay, covering the complete development process, key urpay app features, technology stack, and costs involved in creating a successful fintech app like Urpay.

What is the urpay App?

Urpay is a digital wallet and fintech application that allows users to manage money, make payments, transfer funds, and access financial services directly from their smartphones. It is developed by Neoleap, a subsidiary of Arab National Bank, and is widely used in Saudi Arabia as part of the country’s shift toward a cashless digital economy.

Key Functions of Urpay App:

- Digital wallet for storing and managing money

- Instant local and international money transfers

- Bill payments (electricity, water, telecom, etc.)

- QR code-based payments in stores

- Virtual and physical Mada & Visa cards

- Mobile recharge and e-SIM services

- Online shopping and in-app purchases

- Salary and family payment management

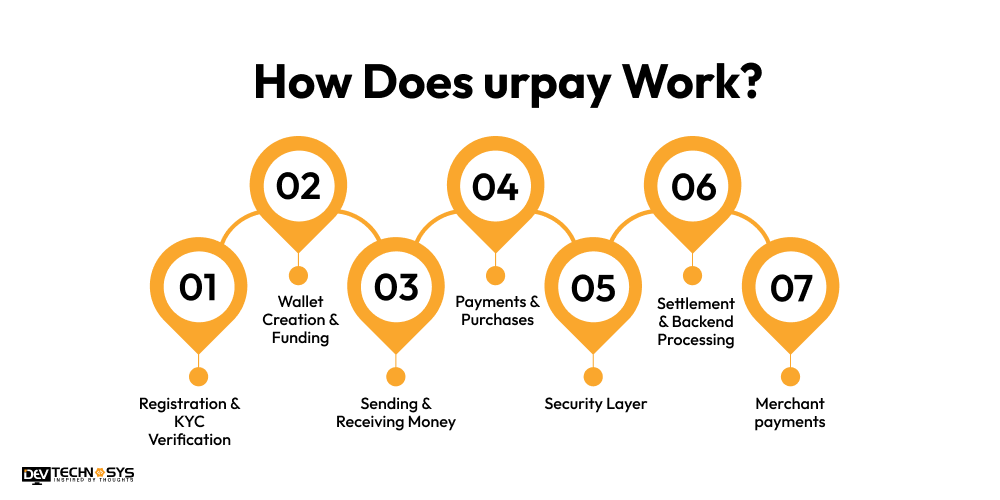

How Does urpay Work?

Top Fintech Apps in Middle East, such as Urpay, is a secure digital wallet that enables users to manage money, make payments, and transfer funds instantly through a single mobile application. Here’s how it functions:

1. Registration & KYC Verification

Users sign up using their mobile number and complete KYC verification by submitting identity documents. This ensures regulatory compliance, identity authentication, and secure onboarding into the fintech ecosystem.

2. Wallet Creation & Funding

After verification, a digital wallet is created for the user. Funds can be added via bank transfer, debit/credit cards, or linked bank accounts to enable seamless financial transactions.

3. Sending & Receiving Money

Users can instantly send and receive money through P2P transfers, bank account payouts, or supported international remittance channels, ensuring fast, secure, and real-time digital financial movement.

4. Payments & Purchases

Mobile app development company integrates wallet supports online shopping, QR-based in-store payments, bill payments, and mobile recharges, for users to complete everyday transactions without relying on physical cash or traditional banking methods.

5. Security Layer

Similar app like urpay secures transactions using encryption, OTP verification, biometric authentication, and advanced fraud detection systems, ensuring every payment is protected against unauthorized access, cyber threats, and suspicious financial activities.

6. Settlement & Backend Processing

Behind the scenes, Urpay integrates with banking networks, payment gateways, and financial institutions to process transactions in real time, ensuring accurate settlement, validation, and smooth financial system coordination.

Answer a few quick questions and our experts will share a tailored project estimate.

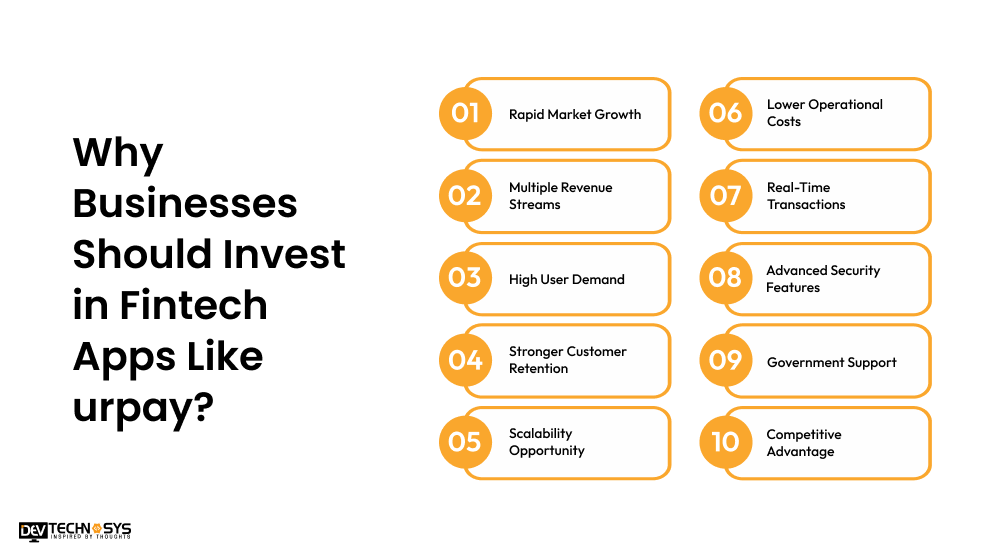

Why Businesses Should Invest in Fintech Apps Like urpay?

Fintech apps are transforming the way people manage money by enabling secure, fast, and cashless digital transactions. urpay is one such platform that simplifies payments, money transfers, and financial management through a single mobile wallet solution.

- Rapid Market Growth: Digital payments and fintech adoption are increasing globally, especially in the Middle East and Asia.

- Multiple Revenue Streams: Earn through transaction fees, subscriptions, FX charges, and merchant commissions.

- High User Demand: Customers prefer all-in-one digital wallets for payments, transfers, and bill management.

- Stronger Customer Retention: The Urpay clone app increase engagement through daily financial usage.

- Scalability Opportunity: Easy to expand into new regions and add financial services over time.

- Lower Operational Costs: Reduces dependency on traditional banking systems and manual processes.

- Real-Time Transactions: Enables instant payments, transfers, and settlements.

- Advanced Security Features: investing to create urpay clone app with AI fraud detection, encryption, and KYC/AML compliance to improve trust.

- Government Support: Many countries promote cashless economies and digital financial ecosystems.

- Competitive Advantage: Helps businesses stay ahead in the evolving digital finance industry.

Fintech App Market Stats 2026 and Beyond

- UAE fintech market size in 2026 is estimated at USD 52.07 billion, with 2031 projections showing USD 90.06 billion, growing at 11.58% CAGR over 2026-2031.

- By service proposition, digital payments commanded 56.88% of UAE fintech market share past year, while insurtech is advancing at a 13.91% CAGR to 2031.

- By end-user, the business segment is expanding at a 12.85% CAGR through 2031.

- By user interface, web browsers are projected to grow at 14.2% CAGR to 2031.

- By Emirate, Dubai led with 59.68% UAE fintech market share last year; Abu Dhabi shows the highest CAGR at 13.74% through 2031.

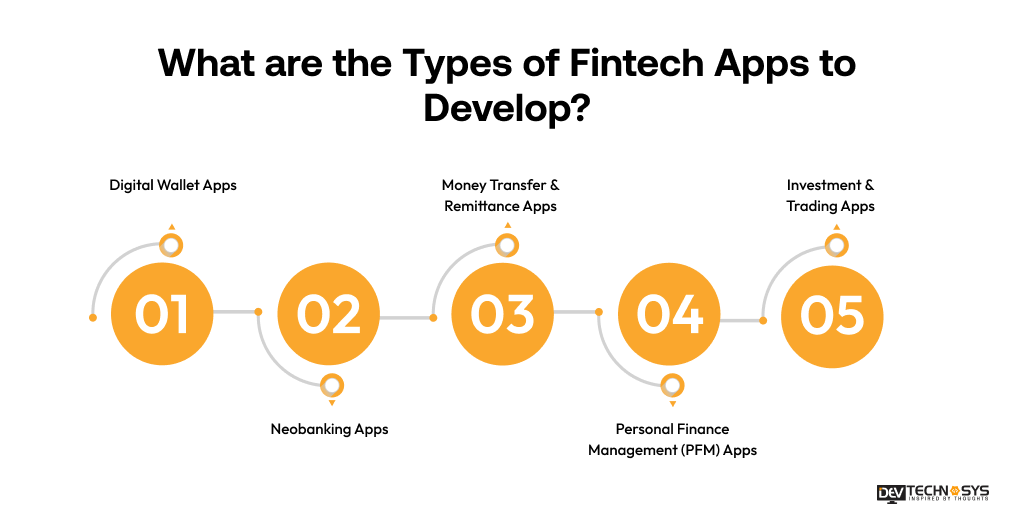

What are the Types of Fintech Apps to Develop?

Fintech is evolving rapidly, and different app categories are reshaping how users manage, invest, and transfer money digitally. Below are the major fintech app types driving global financial transformation.

1. Digital Wallet Apps

Digital wallet apps allow users to store money digitally, make instant payments, transfer funds, and pay merchants using QR codes or mobile numbers. They are widely used for cashless transactions and everyday financial activities.

2. Neobanking Apps

Neobanking apps offer fully digital banking services without physical branches. They provide account management, savings tools, debit cards, and real-time banking features with a seamless mobile-first experience.

3. Money Transfer & Remittance Apps

These apps enable domestic and international money transfers with low fees and fast processing. They are especially important for cross-border payments, migrant workers, and global businesses.

4. Personal Finance Management (PFM) Apps

Android app development experts create PFM apps to help users track expenses, manage budgets, analyze spending patterns, and improve financial planning using AI-driven insights and financial dashboards.

5. Investment & Trading Apps

Investment apps allow users to invest in stocks, crypto, mutual funds, and ETFs. They provide real-time market data, portfolio tracking, and automated investing tools for beginners and advanced traders.

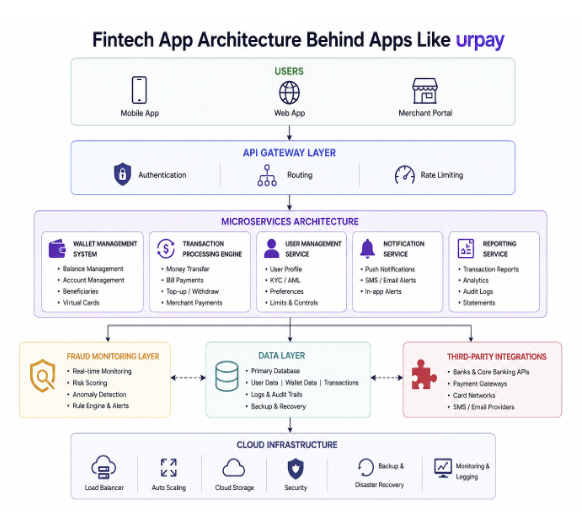

Fintech App Architecture Behind Apps Like urpay

Fintech apps like Urpay are built on a secure, scalable architecture that integrates wallets, payment gateways, and banking APIs to enable real-time digital transactions. Their architecture ensures high performance, security, and compliance while efficiently processing millions of financial transactions.

- Microservices Architecture: Fintech apps are built using microservices to break the system into independent modules like payments, users, wallets, and notifications, ensuring scalability, flexibility, and faster deployment.

- API Gateway Layer: Acts as a central entry point that manages all client requests, routes traffic securely to services, handles authentication, rate limiting, and ensures smooth communication between frontend and backend systems.

- Wallet Management System: Core module that manages user balances, deposits, withdrawals, and ledger entries while ensuring accurate real-time tracking of all financial transactions and account activities.

- Transaction Processing Engine: The urpay clone app includes a transaction processing engine to handle end-to-end payment execution, including authorization, validation, fund transfer, and settlement across banks, payment gateways, and internal wallet systems.

- Fraud Monitoring Layer: Build a Fintech app like Barq that uses AI and rule-based systems to detect suspicious activity, prevent unauthorized transactions, and ensure compliance with KYC/AML regulations for secure financial operations.

Industry Insights

According to statista, the mobile POS payments alone are expected to hit $18.95 trillion in 2026.

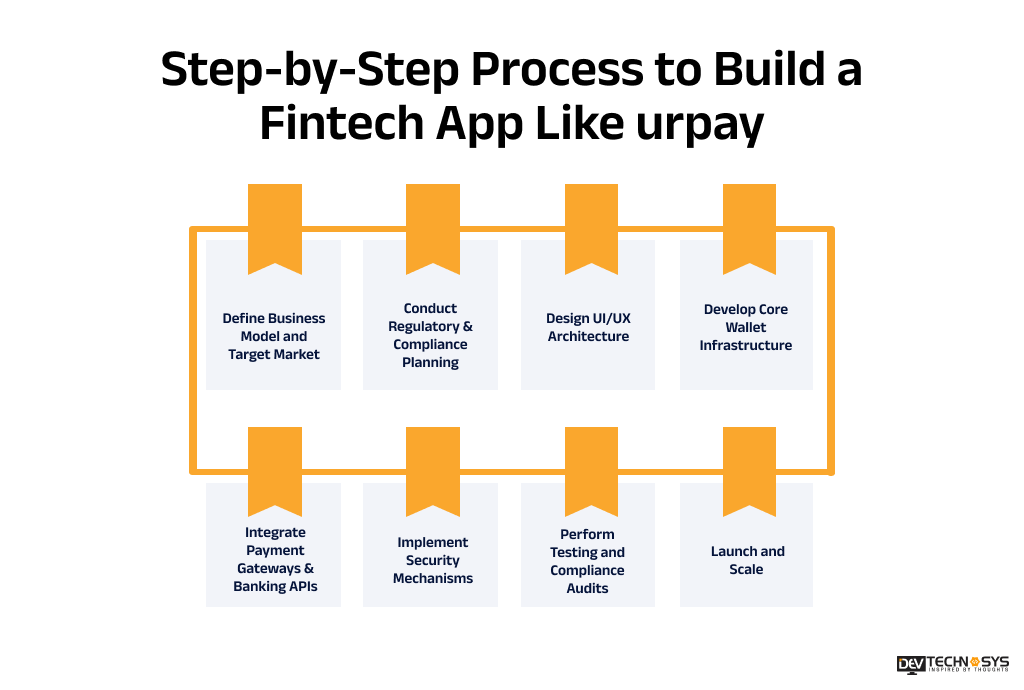

Step-by-Step Process to Build a Fintech App Like urpay

According to experts who provide fintech app development services, building a fintech app like urpay requires a structured approach that combines regulatory compliance, secure architecture, and seamless user experience. A well-defined development process ensures scalability, security, and smooth financial operations from day one.

Step 1: Define Urpay Business Model and Target Market

To build a Fintech app like benefits pay, first you need to Identify your fintech business model, such as transaction fees, subscriptions, or FX margins, and clearly define your target audience, including retail users, SMEs, or cross-border payment customers. This step helps shape product strategy, feature planning, and long-term scalability direction for the platform.

Step 2: Conduct Regulatory & Compliance Planning

Research and comply with financial regulations like KYC, AML, and PCI-DSS based on your target region. Obtain necessary licenses and ensure legal frameworks are in place before development begins to avoid penalties, build trust, and ensure smooth financial operations within regulated banking ecosystems.

Step 3: Design UI/UX Architecture

Hire mobile app developers in Middle East to create a highly intuitive and user-centric design. You should focus on seamless navigation, fast transactions, and simplified financial workflows. A strong UI/UX ensures users can easily manage wallets, send money, and complete payments without friction, improving engagement and retention in competitive fintech markets.

Step 4: Develop Core Wallet Infrastructure

Build the digital wallet backend that manages user accounts, balances, ledger entries, deposits, withdrawals, and real-time transaction updates. This core system must ensure high accuracy, fault tolerance, and scalability as it forms the foundation of all financial operations within the app.

Step 5: Integrate Payment Gateways & Banking APIs

Connect the platform with banking systems, card networks, and third-party payment gateways to enable deposits, withdrawals, transfers, and merchant payments. Hire dedicated developer to add these to ensure interoperability, real-time processing, and seamless financial connectivity across different banking and payment ecosystems globally.

Step 6: Implement Security Mechanisms

Fintech app development solution providers integrate strong security layers, including encryption, multi-factor authentication, biometric verification, and AI-powered fraud detection systems. These mechanisms protect sensitive financial data, prevent unauthorized access, and ensure secure transactions, which is critical for building user trust in fintech applications.

Step 7: Perform Testing and Compliance Audits

Conduct extensive functional, performance, security, and load testing to ensure system stability. Additionally, perform compliance audits to verify adherence to regulatory standards, identify vulnerabilities, and ensure the application is fully ready for real-world financial operations.

Step 8: Launch and Scale

Deploy the fintech application into production and continuously monitor performance, user behavior, and system stability. Gradually scale infrastructure, optimize transaction handling, and introduce new urpay app features to expand into new markets and support growing user demand efficiently.

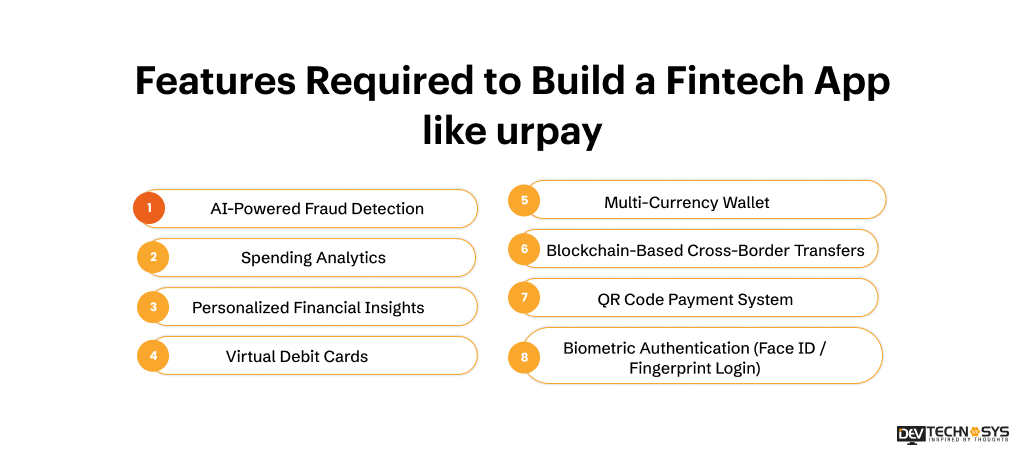

Features Required to Build a Fintech App like urpay

User Panel Features |

Merchant Features |

Admin Panel Features |

| User registration | Payment acceptance | User management |

| Biometric authentication | QR generation | Transaction monitoring |

| Wallet management | Analytics dashboard | Compliance controls |

| Bank account linking | Settlement management | Fraud detection |

| P2P transfers | Invoice generation | KYC verification management |

| QR code payments | Refund processing | Role & permission control |

| Transaction history | Multi-payment support | Dispute management |

| Push notifications | Loyalty & cashback offers | System configuration & reporting |

| Profile management | Transaction tracking tools | Audit logs monitoring |

| Multi-currency support | Merchant onboarding | AML monitoring system |

| PIN/OTP security | Payment link generation | Risk scoring engine |

| Beneficiary management | Subscription billing | Notification management system |

1. Spending Analytics

Build a Fintech app like Pyypl that provides detailed, real-time breakdown of user expenses across categories such as food, travel, and utilities, helping users understand spending behavior, identify financial patterns, and make smarter budgeting and saving decisions effectively.

2. Personalized Financial Insights

Uses advanced AI and machine learning to analyze transaction history and user behavior, delivering tailored financial recommendations, budgeting suggestions, savings opportunities, and actionable insights to improve overall financial health and decision-making.

3. Virtual Debit Cards

Enables instant generation of secure digital debit cards linked to wallet balances, allowing safe online transactions, subscription payments, and enhanced control over spending limits without exposing physical card details or banking information.

4. Multi-Currency Wallet

Supports storing, managing, and transacting in multiple global currencies within a single wallet, enabling seamless international payments, real-time currency conversion, and reduced dependency on traditional forex systems or banking intermediaries.

5. Blockchain-Based Cross-Border Transfers

Leverages blockchain technology to facilitate fast, secure, and transparent international money transfers, reducing transaction costs, eliminating intermediaries, and ensuring traceable, near-instant settlements across global financial networks.

6. QR Code Payment System

Allows users and merchants to perform instant, contactless payments by scanning QR codes, streamlining in-store transactions, peer-to-peer transfers, and enhancing checkout efficiency with secure and frictionless payment experiences.

7. Biometric Authentication (Face ID / Fingerprint Login)

Enhances app security by enabling users to access accounts and authorize transactions using fingerprint or facial recognition, ensuring strong identity verification, fraud prevention, and protection against unauthorized access attempts.

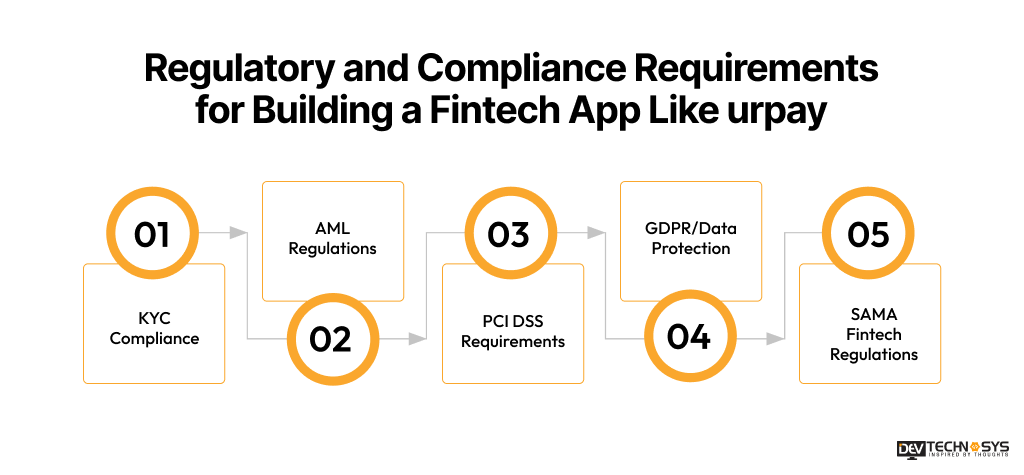

Regulatory and Compliance Requirements for Building a Fintech App Like urpay

Fintech apps like urpay must comply with strict regulatory frameworks to ensure secure, transparent, and legally approved financial operations. These compliance standards form the backbone of trust, security, and risk management in digital financial ecosystems.

1. KYC Compliance (Know Your Customer)

To build a Fintech app like Pyypl, ensuring KYC is crucial. It ensures proper user identity verification during onboarding using government-issued IDs, biometric checks, and document validation. It helps prevent identity fraud, ensures legitimate user access, and is mandatory for maintaining regulatory approval in fintech ecosystems globally.

2. AML Regulations (Anti-Money Laundering)

AML frameworks monitor transactions to detect suspicious activities such as money laundering, terrorism financing, or illegal fund transfers. Fintech apps must implement real-time monitoring systems, risk scoring, and reporting mechanisms to comply with financial intelligence authorities.

3. PCI DSS Requirements

PCI DSS compliance ensures secure handling of credit and debit card data within payment systems. It requires encryption, secure networks, vulnerability management, and strict access control policies to protect sensitive financial information during transactions.

4. GDPR / Data Protection

Data protection laws like GDPR regulate how user data is collected, stored, and processed. Fintech apps must ensure user consent, data encryption, right-to-access controls, and secure storage to protect privacy and avoid legal penalties.

5. SAMA Fintech Regulations

SAMA regulations govern fintech operations in Saudi Arabia, requiring licensing, capital requirements, cybersecurity standards, and compliance reporting. These rules ensure financial stability, consumer protection, and secure digital payment ecosystem development within the region.

Industry Insights

According to Reddit, Instant payment systems like UPI (India) handle 18+ billion transactions per month, making them the world’s largest real-time payment networks.

What are the Top 5 urpay Alternatives to Explore in 2026?

Here are some of the leading digital wallets and urpay alternatives in the Middle East offering similar services like payments, transfers, and digital banking.

App Name |

Launch Year |

Ratings (Avg.) |

Platform Availability |

| Payit by FAB | 2018 | 4.4/5 | Android, iOS |

| e& money | 2022 | 4.3/5 | Android, iOS |

| Careem Pay | 2020 | 4.5/5 | Android, iOS |

| STC Bank | 2018 | 4.6/5 | Android, iOS |

| Tiqmo | 2021 | 4.2/5 | Android, iOS |

1. Payit by FAB

Payit by FAB is a UAE-based digital wallet enabling instant peer-to-peer transfers, bill payments, and merchant transactions. It is one of the best urpay alternatives that is fully integrated with First Abu Dhabi Bank, offering secure, fast, and regulated digital financial services.

2. e& money

e& money is a digital financial app in the UAE providing money transfers, bill payments, and savings tools. It is part of the e& ecosystem, focusing on seamless mobile-first financial experiences and user convenience.

3. Careem Pay

Careem Pay is embedded within the Careem super app, allowing users to send money, pay bills, and manage digital wallets. It supports seamless transactions across ride-hailing, food delivery, and other integrated services.

4. STC Pay

STC Bank (formerly STC Pay) is a leading Saudi digital wallet and neobanking platform that enables users to send money, pay bills, shop online, and manage finances. Build an Fintech app like STC Pay that supports instant transfers, secure payments, and integrated banking services aligned with Saudi Arabia’s cashless economy vision.

5. Tiqmo

Tiqmo is a Saudi digital wallet providing P2P transfers, merchant payments, and financial services. It focuses on simplifying digital transactions for individuals and businesses while promoting cashless payment adoption across the Kingdom.

Technology Stack Required for urpay App Development

Building a fintech app like Urpay requires a robust technology stack that ensures security, scalability, performance, and seamless financial transactions. Choosing the right technologies helps support real-time payments, regulatory compliance, and long-term platform growth.

Component |

Technologies |

| Frontend | Flutter, React Native |

| Backend | Node.js, Django, Spring Boot |

| Database | PostgreSQL, MongoDB |

| Cloud | AWS, Azure, Google Cloud |

| Security | OAuth 2.0, MFA, AES-256 |

| Payments | Stripe, HyperPay, PayTabs |

| Analytics | Firebase, Mixpanel |

Industry Insights

The World Bank states that account ownership in developing economies increased by over 30 percentage points in the last decade.

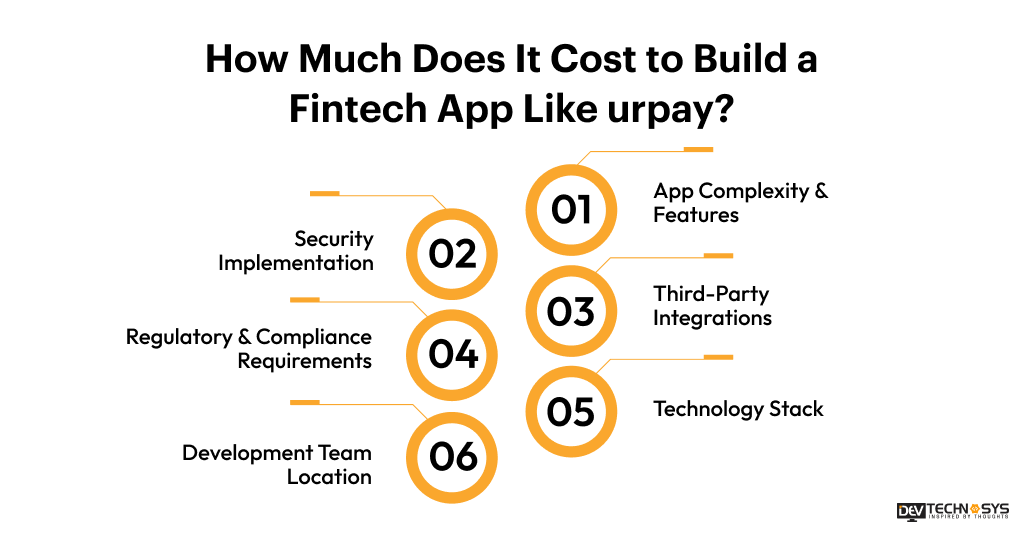

How Much Does It Cost to Build a Fintech App Like urpay?

The cost to build a fintech app like urpay is estimated between $30,000 to $1,50,000. The total cost generally depends on factors like features and complexity, security implementation, third-party integrations, and more.

The basic Fintech mobile app development cost ranges between $30,000 to $60,000.

The mid-range urpay app development cost typically lies between $60,000 to $100,000

The cost to build a fintech app like urpay with advanced features and functionalities like spending analytics, virtual debit cards, multi-currency wallet, exceed to $1,50,000+

App Complexity |

Timeline |

Estimated Cost |

| Basic Fintech MVP | 3–4 Months | $30,000 – $60,000 |

| Mid-Level Fintech App | 4–7 Months | $60,000 – $100,000 |

| Enterprise-Grade Fintech Platform | 7–12+ Months | $100,000 – $150,000+ |

Now let’s move on and learn a little bit about the factors that impact the cost to develop a fintech app like urpay significantly.

1. App Complexity & Features

The number and complexity of features directly impact the fintech app development cost. Advanced functionalities such as digital wallets, QR payments, virtual cards, multi-currency support, and cross-border transfers require additional development effort, testing, and infrastructure, increasing both project timelines and overall investment.

2. Security Implementation

Security is a critical component of fintech applications. Features such as end-to-end encryption, biometric authentication, AI-powered fraud detection, multi-factor authentication, and real-time monitoring systems require specialized expertise. It results in a significant increase in cost to develop a fintech app like urpay.

3. Third-Party Integrations

Fintech platforms rely on various external services, including banking APIs, payment gateways, KYC/AML verification providers, currency exchange services, and blockchain networks. Integrating and maintaining these services often involves licensing fees, development costs, and ongoing operational expenses.

4. Regulatory & Compliance Requirements

Compliance with financial regulations such as KYC, AML, PCI-DSS, GDPR, and regional fintech laws requires extensive planning, legal consultation, security audits, and documentation. Meeting these requirements adds both upfront and ongoing costs but is essential for market entry.

5. Technology Stack

The choice of technology significantly affects the cost to develop a fintech app like urpay heavily. Modern technologies such as microservices architecture, cloud-native infrastructure, AI-powered analytics, and blockchain integration improve scalability and performance but require specialized developers and more sophisticated infrastructure investments.

6. Development Team Location

Development and mobile app maintenance costs vary considerably depending on the team’s geographic location. Developers in North America and Western Europe generally charge higher rates, while offshore teams in regions such as India, the UAE, and Eastern Europe often provide more cost-effective development services.

Cost Factor |

Estimated Timeline Impact |

Estimated Cost Contribution (USD) |

| App Complexity & Features | 6 to 16 Weeks | $8,000 – $45,000 |

| Security Implementation | 3 to 8 Weeks | $5,000 – $25,000 |

| Third-Party Integrations | 2 to 6 Weeks | $3,000 – $20,000 |

| Regulatory & Compliance Requirements | 2 to 8 Weeks | $4,000 – $18,000 |

| Technology Stack Selection | 14 Weeks | $4,000 – $15,000 |

| Development Team Location | Affects Entire Project Duration | $6,000 – $27,000 |

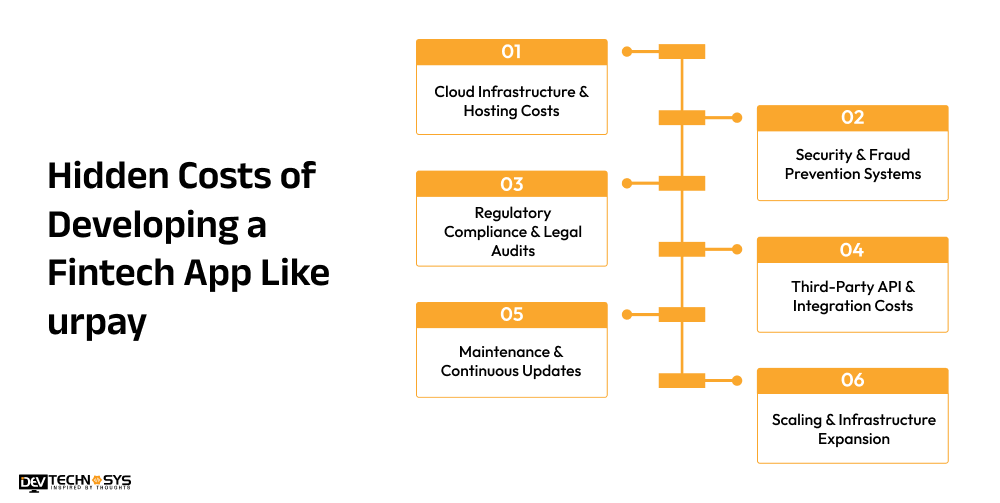

Hidden Costs of Developing a Fintech App Like urpay

While the initial development budget is important, businesses must also account for ongoing operational expenses that arise after launch. These hidden costs can significantly impact the total cost of ownership and are essential for maintaining a secure, scalable, and compliant fintech platform.

1. Cloud Infrastructure & Hosting Costs

Fintech apps require reliable cloud infrastructure to support real-time transactions, data storage, backups, and high availability. As user activity grows, cost to create a fintech app like urpay including the servers, databases, content delivery networks (CDNs), and cloud services, increases accordingly.

2. Security & Fraud Prevention Systems

Protecting sensitive financial data requires continuous investment in encryption technologies, fraud detection tools, penetration testing, threat monitoring, and cybersecurity upgrades. These measures help prevent data breaches, unauthorized transactions, and financial fraud.

3. Regulatory Compliance & Legal Audits

Fintech companies must regularly conduct compliance audits and maintain adherence to regulations such as KYC, AML, PCI-DSS, and regional financial laws. Legal consultations, certification renewals, and regulatory reporting impact the cost to create a fintech app like urpay.

4. Third-Party API & Integration Costs

Many hybrid app development services depend on external providers for payment processing, identity verification, banking connectivity, currency exchange, and fraud detection. Most of these services charge recurring subscription fees, usage-based costs, or transaction-based pricing.

5. Maintenance & Continuous Updates

Regular maintenance is required to fix bugs, improve performance, introduce new features, and ensure compatibility with evolving operating systems and devices. Most businesses allocate a dedicated annual budget to keep the application updated and competitive.

6. Scaling & Infrastructure Expansion

As the platform gains more users and processes higher transaction volumes, businesses must invest in additional servers, database optimization, load balancing, and performance enhancements. These scalability costs become increasingly important as the fintech ecosystem grows.

Hidden Cost Factor |

Estimated Impact on Total Cost |

Typical Cost Range |

| Cloud Infrastructure & Hosting | +5% to +12% | $2,000 – $15,000/year |

| Security & Fraud Prevention Systems | +8% to +15% | $3,000 – $20,000/year |

| Regulatory Compliance & Legal Audits | +5% to +10% | $2,000 – $15,000/year |

| Third-Party API & Integration Costs | +5% to +12% | $2,000 – $18,000/year |

| Maintenance & Continuous Updates | +15% to +25% | $4,500 – $37,500/year |

| Scaling & Infrastructure Expansion | +10% to +20% | $5,000 – $30,000/year |

Monetization Strategies for a Fintech App Like urpay

Fintech apps generate revenue through multiple channels by offering payment services, financial products, and premium features. A diversified monetization model helps ensure sustainable growth while maximizing user lifetime value.

1. Transaction Fees

Charge users a small fee for specific transactions such as instant transfers, international remittances, bill payments, or wallet withdrawals. Even minimal transaction charges can generate significant revenue when processed across a large and active user base.

2. Merchant Commission

Earn commissions from merchants for every successful payment processed through the platform. This model creates a win-win ecosystem where merchants gain access to digital customers while the fintech platform generates recurring transaction-based revenue.

3. Subscription Plans

Offer premium membership plans that provide benefits such as higher transaction limits, faster transfers, exclusive rewards, advanced analytics, and priority customer support. Subscription revenue creates a predictable and recurring income stream for the business.

4. Currency Exchange Margins

Generate revenue by applying a small markup on foreign exchange rates during international transfers and multi-currency transactions. This strategy is particularly profitable for fintech apps serving global users and cross-border payment markets.

5. Premium Financial Services

Monetize through value-added financial services such as lending, investment tools, wealth management, insurance products, virtual cards, and business payment solutions. These premium offerings increase revenue while enhancing the overall customer experience and platform value.

Future Trends Shaping Fintech Apps Like urpay

As digital finance continues to evolve, emerging technologies are reshaping how fintech platforms operate, deliver services, and engage users. Businesses that embrace these innovations can gain a competitive edge while meeting the growing demand for smarter and more accessible financial solutions.

1. AI-Powered Finance

AI in Fintech app development is transforming the industry through automated budgeting, personalized financial advice, predictive analytics, and real-time fraud detection. AI-driven systems help users make informed financial decisions while enabling fintech providers to improve operational efficiency and risk management.

2. Open Banking APIs

Open Banking allows secure data sharing between banks and third-party applications through APIs. This trend enables fintech platforms to offer personalized financial services, account aggregation, faster payments, and enhanced customer experiences without relying solely on traditional banking systems.

3. Embedded Finance

Embedded finance integrates financial services directly into non-financial platforms such as e-commerce apps, ride-hailing services, and marketplaces. Users can access payments, lending, insurance, and banking services seamlessly within the apps they already use every day.

4. CBDCs and Digital Currencies

Central Bank Digital Currencies (CBDCs) are emerging as government-backed digital alternatives to cash. As adoption grows, fintech apps may integrate CBDCs alongside traditional currencies, enabling faster transactions, greater transparency, and improved financial inclusion.

5. Blockchain-Based Payments

Blockchain technology is revolutionizing payment systems by enabling secure, transparent, and near-instant transactions. Fintech platforms are increasingly leveraging blockchain for cross-border transfers, smart contracts, and decentralized financial services while reducing costs and settlement times.

Build vs Buy vs Development Partner: Which Option is More Cost-Effective for Businesses?

When developing a fintech solution like urpay, businesses typically choose between building in-house, buying a ready-made solution, or partnering with a development company. Each approach varies significantly in cost, time, scalability, and control.

- Build In-House: Maximum control and customization, but the highest cost and longest timeline. Suitable for large enterprises with strong technical teams.

- Buy Ready Solution: Fastest and cheapest option, but limited customization and scalability. Best for MVPs or quick market entry.

- Development Partner: Balanced approach offering expert execution, faster delivery, and moderate cost. Ideal for startups and scaling fintech businesses.

Factor |

Build In-House |

Buy Ready-Made Solution |

Development Partner |

| Estimated urpay app cost (USD) | $120,000 – $150,000 | $30,000 – $60,000 | $60,000 – $120,000 |

| Development Timeline | 9 to 12 months | 1 to 2 months | 4 to 8 months |

| Customization Level | Very High | Low | High |

| Scalability | High | Limited | High |

| Speed to Market | Slow | Very Fast | Moderate |

| Control & Ownership | Full Control | Limited Control | Shared Control |

| Technical Expertise Needed | Very High | Minimal | Moderate |

| Compliance Readiness | Internal Effort Required | Pre-built but limited | Included with expertise |

Conclusion

Building a fintech app like Urpay requires a strong combination of secure architecture, regulatory compliance, and user-centric design. From defining the business model and selecting the right technology stack to integrating banking APIs, implementing fraud prevention systems, and ensuring KYC/AML compliance, every stage plays a critical role in success.

If you are a business looking for a top fintech app development company, look no further than Dev Technosys. With 15+ years of experience and 370+ developers and technical experts, we create top-notch fintech apps like Urpay for businesses of every scale.

FAQs

Q1. Mistakes to Avoid When Building a Digital Wallet App

One of the most common mistakes while building a fintech app like urpay is ignoring regulatory compliance such as KYC and AML requirements. Other pitfalls include weak security implementation, poor UI/UX design, lack of scalability planning, and insufficient third-party integration testing, which can lead to system failures and low user trust.

Q2. Security Framework Used by Digital Wallet Apps

Digital wallet apps typically use multi-layer security frameworks including end-to-end encryption, tokenization, biometric authentication, multi-factor authentication (MFA), and AI-based fraud detection systems. These layers ensure secure transactions, prevent unauthorized access, and protect sensitive financial and user data in real time.

Q3. SAMA Compliance Checklist for Fintech Startups

To operate in Saudi Arabia, fintech startups must create online payment app that follows SAMA guidelines, including licensing approval, AML/KYC implementation, cybersecurity standards, data protection policies, transaction monitoring systems, and regular audits. Compliance ensures legal operation, financial transparency, and consumer protection within the Saudi fintech ecosystem.

Q4. Which Countries Accept Urpay?

Urpay QR code payment app is primarily designed for use within Saudi Arabia, supporting domestic payments, a P2P payment solution, banking services, and local transactions. Its usage outside the country is limited, depending on merchant acceptance and cross-border banking or transfer integrations.

Q5. How Long Does it Take to Build a Fintech App Like Urpay?

The development timeline typically ranges from 3 to 12 months, depending on complexity, features, and compliance requirements. A basic MVP can be built in 3 to 4 months, while a fully scalable, enterprise-grade contactless payment app with advanced security and integrations may take 7 to 12 months or more.

{kind=link}