Key Takeaways

The cost to build a BNPL app typically ranges from $30,000 to $150,000+, depending on app complexity, features, platform selection, compliance requirements, security standards, and integration needs. Additional factors such as ongoing maintenance, cloud infrastructure, and third-party API fees also influence the final budget.

Cost Based on App Complexity

- Basic BNPL MVP($30,000 – $50,000): Includes core lending features, basic onboarding, and simple repayment tracking to validate the business idea quickly.

- Mid-Level BNPL App($50,000 – $90,000): Includes merchant dashboards, payment integrations, notifications, and moderate customization.

- Advanced BNPL Platform($90,000 – $120,000): Includes credit assessment engines, fraud detection, financial analytics, and stronger compliance features.

- Enterprise BNPL Solution($120,000 – $150,000+): Includes open banking integration, multi-region deployment, AI-driven underwriting, and high scalability.

Cost Based on Platform Selection

- Android BNPL App Development($25,000 – $90,000+): Supports a wide user base but requires extensive testing across device fragmentation.

- iOS BNPL App Development($25,000 – $85,000+): Offers a controlled ecosystem with smoother testing and premium user targeting.

- Cross-Platform BNPL Development($30,000 – $100,000+): Uses a shared codebase to reduce cost and speed up launch through frameworks like Flutter or React Native.

Cost Based on BNPL App Type

- Madfu or Sympl-like App($40,000 – $85,000): Covers basic lending features, user verification, and flexible repayment plans.

- Postpay-like App($50,000 – $90,000): Covers installment management, merchant onboarding, and payment tracking.

- Tabby or Tamara-like App($60,000 – $110,000): Covers multi-merchant ecosystems, advanced underwriting, and large-scale analytics.

The cost to build a BNPL app typically ranges from $15,000 to $80,000 or more, depending on the platform you choose, the features you include, payment integrations, and the compliance requirements you need to meet. Simple MVPs sit at the lower end, while full-scale, multi-market lending platforms with advanced credit engines can cost significantly more.

Pricing also depends heavily on security architecture, KYC and AML compliance, credit underwriting logic, fraud detection systems, and third-party payment gateway integrations. Scalability for growing transaction volumes matters too, especially for multi-merchant retail platforms. Each additional layer of functionality adds development hours, infrastructure cost, and ongoing maintenance and support overhead.

In this guide, you’ll find a detailed cost breakdown, must-have features, hidden expenses, realistic timelines, and monetization strategies for BNPL app development planning, so you can budget and plan with confidence.

What is a BNPL App and How Does It Work?

A BNPL app is a digital financing platform that allows customers to purchase products immediately and pay for them later through scheduled installments. The customer checks out without paying the full amount upfront. The merchant still receives payment in full, while the BNPL provider collects repayments directly from the customer over time. This is the core model behind most BNPL app development projects today.

Key Components of a BNPL Platform

Behind every transaction sits a layered system. User onboarding verifies identity, KYC checks confirm eligibility, and credit assessment engines evaluate repayment risk in real time. A merchant dashboard tracks sales and payouts, while repayment management handles installment schedules and reminders. Businesses investing in a BNPL app development solution must integrate these systems alongside secure payment gateways to support smooth digital lending operations. This level of BNPL application development directly shapes consumer financing outcomes and overall platform reliability.

Industry Insight

According to the Bank for International Settlements (BIS), “Buy Now, Pay Later products blur the boundary between payments and credit, creating new regulatory challenges in consumer protection and credit risk assessment.”

How Much Does It Cost to Build a BNPL App in 2026?

The cost to build a BNPL app generally falls between $30,000 and $150,000, depending on your feature set, compliance needs, and platform complexity. A basic MVP costs far less than an enterprise-grade lending platform with advanced credit engines and multi-market support.

Businesses seeking professional BNPL app development services should budget according to their feature requirements and scalability goals. The cost to develop a BNPL app becomes clearer once broken down by app type, as shown below.

| BNPL App Type | Development Cost | Best For | Estimated Timeline |

| Basic BNPL MVP | $30,000 – $50,000 | Startups validating a business idea | 2-3 Months |

| Mid-Level BNPL App | $50,000 – $90,000 | Growing fintech startups and retailers | 4-6 Months |

| Advanced BNPL Platform | $90,000 – $120,000 | Established lending businesses | 6-8 Months |

| Enterprise BNPL Solution | $120,000 – $150,000+ | Banks, large fintech firms, enterprises | 8+ Months |

Answer a few quick questions and our experts will share a tailored project estimate.

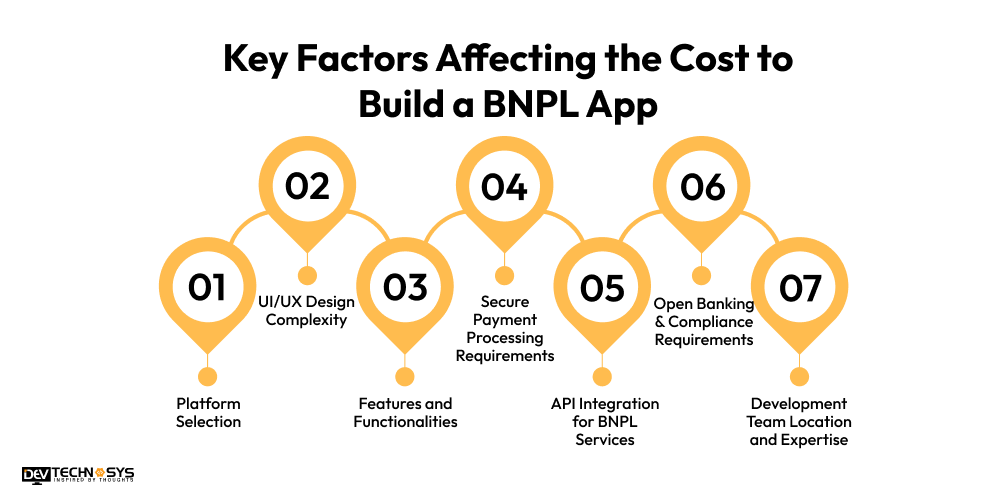

Key Factors Affecting the Cost to Build a BNPL App

The cost to build a BNPL app depends on several technical, business, and compliance variables rather than a single fixed rate. Platform choice, design complexity, feature depth, security standards, and team expertise all shift the final number. Understanding these factors helps businesses set a realistic development budget before starting the project.

1. Platform Selection (Android, iOS, or Cross-Platform)

Choosing Android only or iOS only typically keeps costs lower since development focuses on a single codebase. Building for both platforms increases cost due to parallel design and testing efforts. Many businesses reduce expenses by opting for cross-platform frameworks instead of separate native builds. For Android-first launches, Android app development remains a cost-efficient starting point for many fintech founders.

2. UI/UX Design Complexity

Financial apps need interfaces that build trust quickly, since users are sharing sensitive data and committing to repayments. Custom design work, intuitive onboarding flows, and clean dashboard layouts all add development hours. The more complex the merchant and customer dashboards become, the higher the cost to create a BNPL app climbs, especially when multiple user roles need distinct views.

3. Features and Functionalities

Core functionality drives a large share of the budget. KYC verification, credit scoring, repayment tracking, merchant management, push notifications, and analytics dashboards each require dedicated development effort and testing. A well-structured BNPL app development solution typically bundles these features together, but each additional module, such as advanced fraud scoring or custom reporting, adds incremental cost and timeline.

4. Secure Payment Processing Requirements

Every BNPL platform handles real money movement, so security cannot be an afterthought. Costs rise with the need for secure payment gateways, end-to-end encryption, and PCI DSS compliance. Transaction security measures, including tokenization and fraud monitoring, also add to development effort but are non-negotiable for protecting customer data and maintaining regulatory trust.

5. API Integration for BNPL Services

Most BNPL platforms rely on third-party APIs rather than building everything in-house. API integration for BNPL apps typically includes banking APIs for fund transfers, credit scoring APIs for risk assessment, identity verification APIs for KYC, and payment APIs for checkout. Each integration adds licensing fees, testing time, and ongoing maintenance to the overall budget.

6. Open Banking & Compliance Requirements

Regulatory compliance shapes both cost and development timeline significantly. Open banking integration allows secure access to customer financial data with proper consent, but it requires strict adherence to data protection standards and financial reporting obligations. Building this infrastructure correctly from the start avoids costly rework later and keeps the platform aligned with regional lending regulations.

7. Development Team Location and Expertise

Where you hire your team has a major impact on the final cost. Developers in the US and Europe typically charge premium rates, while teams in the UAE and offshore hubs often deliver comparable quality at lower rates. Many fintech founders choose to hire dedicated developer teams with proven BNPL experience to balance cost control with technical reliability and faster delivery.

| Cost Factor | Low-End Cost Impact | High-End Cost Impact |

| Platform Selection (Android, iOS, or Cross-Platform) | $5,000 | $20,000 |

| UI/UX Design Complexity | $4,000 | $18,000 |

| Features and Functionalities | $10,000 | $50,000 |

| Secure Payment Processing Requirements | $4,000 | $20,000 |

| API Integration for BNPL Services | $4,000 | $20,000 |

| Open Banking & Compliance Requirements | $3,000 | $22,000 |

BNPL App Development Cost Breakdown by Development Stage

BNPL app development moves through several distinct stages, from initial planning to final deployment. Each stage absorbs a portion of the overall budget, and understanding this distribution helps businesses track spending and avoid cost overruns during the project.

| Development Stage | Estimated Cost Range | Cost Contribution |

| Business Analysis & Planning | $3,000 – $8,000 | 10% |

| UI/UX Design | $4,000 – $12,000 | 15% |

| Frontend Development | $8,000 – $25,000 | 20% |

| Backend Development | $10,000 – $35,000 | 30% |

| Testing & Quality Assurance | $3,000 – $10,000 | 10% |

| Deployment & Launch | $2,000 – $8,000 | 5% |

| Security & Compliance Setup | $5,000 – $20,000 | 10% |

1. Business Analysis & Planning

This stage covers requirement gathering, market research, and feature planning before any code is written. Teams also define the technical architecture early on, ensuring the platform can scale as transaction volumes and user numbers grow over time.

2. UI/UX Design

Designers create wireframes and map out user journeys for both customers and merchants. Financial dashboards need extra attention here, since clarity directly affects trust and repayment behavior. Many businesses partner with a mobile app development company at this stage to ensure the experience feels intuitive from day one.

3. Frontend & Backend Development

Frontend development focuses on building the customer-facing interface and ensuring a smooth checkout and repayment experience. Backend development, which carries the largest cost share, handles credit assessment logic, the repayment engine, merchant management systems, and the database architecture that ties everything together. This stage forms the technical backbone of any serious BNPL application development project.

4. Testing, Security & Deployment

Before launch, teams run bug fixes and performance testing across devices and load conditions. Security audits and compliance checks confirm the platform meets fintech standards, particularly around secure payment processing and data protection. Once testing clears, the app moves into production deployment and ongoing monitoring.

Industry Insight

According to the Financial Conduct Authority (FCA), “Lenders must carry out affordability checks to make sure customers can afford to repay BNPL before offering it.”

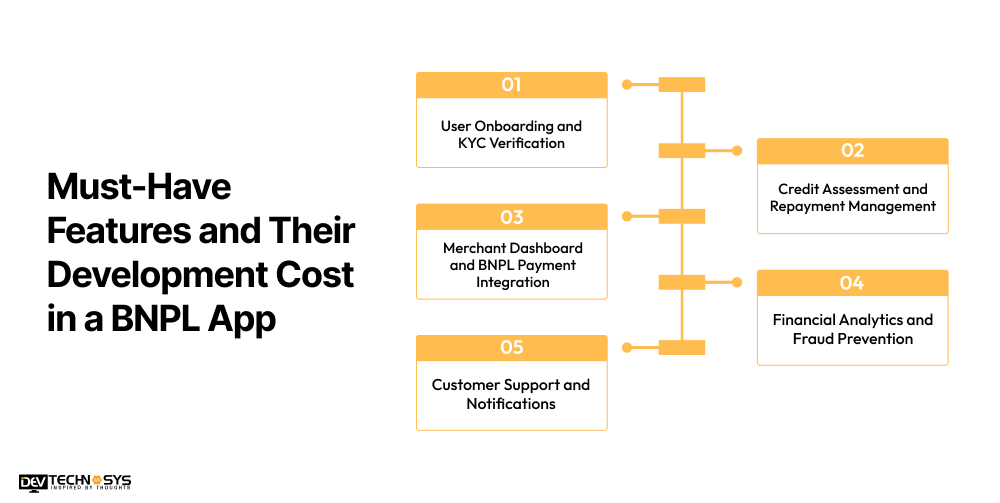

Must-Have Features and Their Development Cost in a BNPL App

The final Buy Now Pay Later app cost largely depends on which features make it into the platform. Basic functionality, like login and notifications, adds modest cost, while advanced capabilities, such as credit assessment, repayment management, and fraud prevention, significantly increase the overall cost to build a BNPL app.

1. User Onboarding and KYC Verification

Account creation needs to be quick, but identity verification still has to satisfy regulatory compliance. This stage covers customer authentication and document checks that confirm a user’s identity before any credit decision is made, forming the foundation of reliable BNPL application development.

2. Credit Assessment and Repayment Management

Credit checks determine whether a customer qualifies for installment financing, while eligibility evaluation sets their spending limits. Once approved, the system generates installment schedules and tracks every payment against them. This logic sits at the core of digital lending app development and directly affects default rates.

4. Merchant Dashboard and BNPL Payment Integration

Merchants need visibility into transaction tracking, payment settlements, and order monitoring from a single dashboard. Smooth BNPL payment integration ensures merchants receive funds upfront while customers repay in installments behind the scenes. Businesses building this layer often turn to established BNPL app development services to get merchant onboarding right from launch.

5. Financial Analytics and Fraud Prevention

Spending analysis and customer behavior tracking help businesses understand usage patterns and repayment risk over time. Financial data analytics also feeds risk monitoring models, while a dedicated fraud detection system flags suspicious transactions before they cause losses, protecting both the platform and its users.

6. Customer Support and Notifications

Payment reminders and due-date alerts reduce missed installments and keep customers informed without manual follow-up. A responsive customer support module handles disputes and account questions, which together improve user engagement and repayment compliance.

Cost to Build a BNPL App Like Popular Market Leaders in UAE

Leading BNPL platforms differ widely in feature depth, lending logic, and integration scope, which directly affects the cost to develop a BNPL app. Businesses can start with a lean MVP or invest in enterprise-grade functionality depending on their long-term growth goals and target market.

| BNPL App | Estimated Development Cost | Complexity Level |

| Tabby-like App | $60,000 – $100,000 | High |

| Tamara-like App | $70,000 – $110,000 | High |

| Postpay-like App | $50,000 – $90,000 | Medium-High |

| Madfu-like App | $40,000 – $80,000 | Medium |

| Sympl-like App | $40,000 – $85,000 | Medium |

| Enterprise BNPL Platform | $120,000 – $150,000+ | Very High |

1. Tabby

A Tabby-style platform requires a multi-merchant ecosystem with advanced underwriting models to support diverse retail partners. The cost to develop a BNPL app at this level rises due to large-scale user support and detailed analytics dashboards that track spending patterns across thousands of merchants.

2. Madfu

Madfu-style platforms focus on basic lending features, straightforward user verification, and clear repayment schedules. Businesses looking to develop a BNPL app like Madfu can launch with a leaner budget while still covering essential compliance and merchant management needs.

3. Tamara

Tamara-style apps focus heavily on retail integrations and flexible customer financing options. Repayment automation and stronger risk assessment models add development complexity, which pushes the cost to create a BNPL app higher compared to simpler installment platforms.

4. Postpay

A Postpay-style app centers on solid installment management, smooth merchant onboarding, and reliable payment tracking. These core capabilities keep development moderately complex without requiring the extensive underwriting layers seen in larger platforms.

5. Sympl

A Sympl-style app emphasizes flexible payment plans, strong merchant partnerships, and simple customer management tools. Teams aiming to build a BNPL app like Sympl typically prioritize scalability considerations early, so the platform can expand its merchant network without a costly rebuild later.

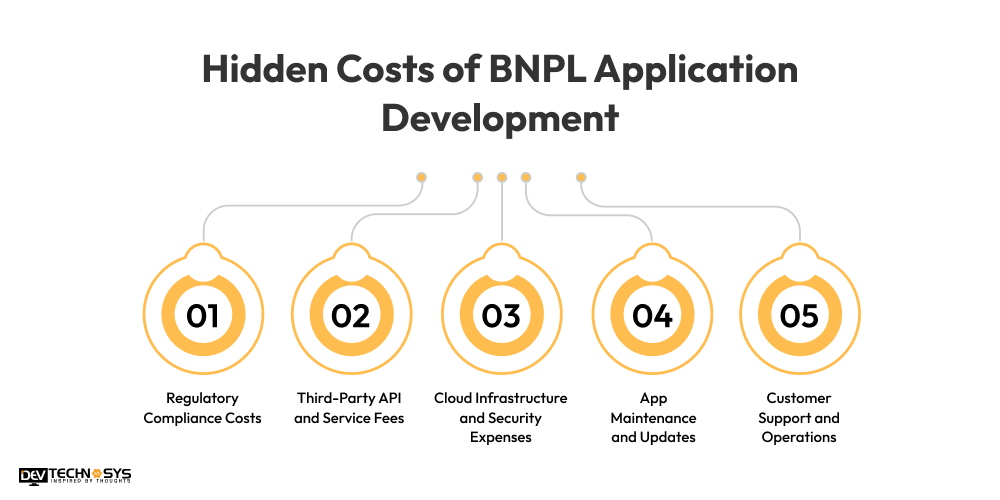

Hidden Costs of BNPL Application Development

Development is only part of the investment. Once you calculate the cost to build a BNPL app, you still need to plan for infrastructure, compliance, security, and ongoing maintenance expenses that surface well after launch.

1. Regulatory Compliance Costs

KYC requirements and data protection regulations demand continuous attention, not a one-time setup. Financial compliance audits and legal documentation often require specialist consultants, adding recurring costs that many founders overlook during initial budgeting.

2. Third-Party API and Service Fees

Payment gateways, identity verification tools, and credit scoring services typically charge per-transaction or subscription fees. API integration for BNPL functionality also includes banking integrations, which carry their own licensing costs that scale as transaction volume grows.

3. Cloud Infrastructure and Security Expenses

Cloud hosting and database management costs rise as your user base expands. Backup systems and continuous security monitoring are essential for secure payment processing, protecting both customer data and transaction integrity around the clock.

4. App Maintenance and Updates

Bug fixes, feature enhancements, and OS compatibility updates require ongoing developer time after launch. Performance optimization also matters as usage grows. Understanding mobile app maintenance costs upfront helps businesses budget realistically instead of being caught off guard post-launch.

5. Customer Support and Operations

Support teams handle merchant onboarding questions, dispute management, and day-to-day user issues. These operational costs directly affect customer retention and shouldn’t be treated as an afterthought once the platform goes live.

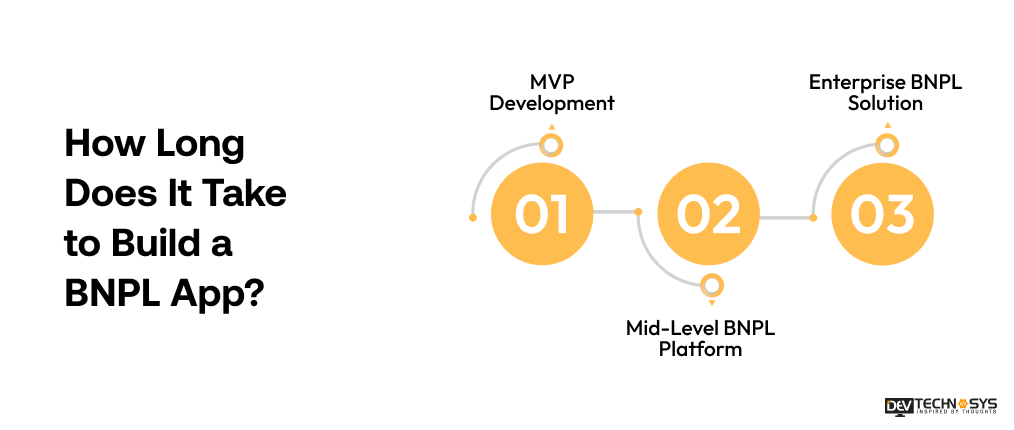

How Long Does It Take to Build a BNPL App?

The development timeline depends on app complexity, feature requirements, third-party integrations, compliance requirements, and testing efforts. BNPL app development for a simple MVP can launch faster, while enterprise-grade platforms require significantly more time to build, test, and deploy.

| BNPL App Type | Estimated Timeline | Key Focus Areas |

| Basic BNPL MVP | 3–4 Months | Core lending features, basic onboarding |

| Mid-Level BNPL App | 4–6 Months | Merchant dashboards, payment integrations |

| Advanced BNPL Platform | 6–8 Months | Analytics, fraud prevention, compliance checks |

| Enterprise BNPL Solution | 8–12 Months | Open banking, multi-region deployment, scalability |

1. MVP Development Timeline

An MVP focuses on core lending features, basic user onboarding, and simple repayment management. This lean scope keeps BNPL MVP development costs lower while allowing businesses to enter the market faster and validate demand.

2. Mid-Level BNPL Platform Timeline

Adding merchant dashboards, analytics, and additional payment integrations extends the timeline. These features require more thorough integration testing before launch, which adds a few extra months compared to a basic MVP.

3. Enterprise BNPL Solution Timeline

Enterprise platforms involve open banking integrations, extensive compliance checks, and robust fraud prevention systems. Scalability assessment and multi-region deployment add further security validation steps, which is why these projects take significantly longer to complete.

Industry Insight

According to the U.S. Consumer Financial Protection Bureau (CFPB), BNPL products are being reviewed under credit regulations to ensure “consumers receive protections similar to those provided for credit cards, including dispute rights and transparency requirements.”

How to Reduce BNPL App Development Cost Without Compromising Quality?

Reducing development expenses does not necessarily mean cutting essential features. Strategic planning, smart technology selection, and phased development can significantly optimize the fintech mobile app development cost while still maintaining strong performance, security, and compliance standards.

1. Start With an MVP

Launching with core features first lets you validate market demand before investing in advanced functionality. This approach keeps BNPL MVP development cost manageable while still gathering real user feedback that guides future scaling decisions.

2. Choose Cross-Platform Development

Building on a single codebase speeds up deployment and lowers ongoing maintenance effort. Many founders turn to hybrid app development services to reach both Android and iOS users without doubling their development budget.

3. Use Ready-Made APIs and Integrations

Instead of building everything from scratch, businesses can rely on existing payment gateways, identity verification tools, and credit scoring services. Solid API integration for BNPL functionality reduces development effort significantly while still meeting security and compliance requirements.

4. Work With Experienced Development Teams

Experienced teams deliver faster with less rework, since they already understand compliance planning and scalable architecture. For region-specific expertise and faster turnaround, founders often hire mobile app developers in UAE markets where fintech experience is growing quickly.

Why Invest in BNPL App Development in 2026?

BNPL has evolved from a simple payment option into a major digital lending solution. Growing eCommerce adoption, changing consumer preferences, and rising demand for flexible payment methods continue to create strong opportunities for fintech startups and retailers entering BNPL app development today.

According to GlobeNewswire industry reports, the global BNPL payment market is expected to grow by 18.9% annually to reach $509.2 billion in 2026, with the sector projected to expand to approximately $1 trillion by 2031.

1. Rising Demand for Flexible Payments

Consumers increasingly prefer installment payments over traditional credit, since they reduce upfront financial burden and increase purchasing power. This shift improves overall customer experience and keeps shoppers returning to platforms that offer flexible checkout options.

2. Expanding Digital Lending Market

Alternative lending continues to grow alongside fintech innovation, increased smartphone adoption, and broader acceptance of digital finance. This momentum makes digital lending app development a timely investment for businesses entering the consumer credit space.

3. Higher Revenue Opportunities for Businesses

Merchants benefit from transaction fees, new partnership opportunities, and stronger customer retention through repeat purchases. Understanding the Buy Now Pay Later app cost upfront helps businesses plan for these long-term revenue streams more accurately.

4. Competitive Advantage in the Fintech Industry

Growing BNPL adoption is opening new market opportunities for brand differentiation and long-term scalability. Partnering with an experienced fintech app development company helps businesses build a platform positioned to compete as the market matures.

Monetization Models for BNPL Apps in 2026?

A successful BNPL platform can generate revenue through multiple income streams rather than relying on a single source. Diversifying monetization strategies helps businesses maximize returns while keeping services attractive to both consumers and merchants throughout BNPL app development.

1. Merchant Transaction Fees

Merchants pay a percentage per transaction, making this the most common BNPL revenue source. In exchange, merchants benefit from increased sales and higher conversion rates, since customers feel more comfortable completing larger purchases. Some platforms structure this similarly to a develop a shop now pay later app model for retail partners.

2. Late Payment Charges

Fees for missed installments create a secondary revenue stream while encouraging timely repayments. These charges must comply with local financial regulations, since excessive penalties can trigger regulatory scrutiny and damage customer trust over time.

3. Subscription and Premium Services

Premium merchant tools and advanced financial data analytics can be offered as paid add-ons. Value-added services like priority support or custom reporting give merchants more reasons to stay within the platform’s ecosystem long-term.

4. Affiliate and Financial Partnerships

Banking partnerships and insurance products open additional referral commission opportunities. Cross-selling financial products, similar to how businesses build an app like Cash Advance, creates sustainable revenue beyond core lending while strengthening customer retention across the platform.

Conclusion

The cost to build a BNPL app typically ranges from $30,000 to $150,000 or more, with the final figure shaped by feature complexity, platform choice, third-party integrations, compliance requirements, and scalability goals. Understanding BNPL app development pricing upfront helps businesses plan budgets realistically and avoid surprises later in the project.

With over 14 years of fintech development experience, Dev Technosys helps businesses build secure, scalable lending platforms from concept to launch. As a trusted BNPL app development company, our team offers end-to-end development support and consultation to help you plan your project with confidence.

Frequently Asked Questions

Q1. How Much Does It Cost to Build a BNPL App From Scratch?

The cost to build a BNPL app typically ranges from $30,000 to $150,000 or more. Final BNPL app development cost depends on app complexity, platform choice, compliance requirements, and integrations. MVP solutions cost significantly less than enterprise-grade platforms.

Q2. What Factors Have the Biggest Impact on BNPL App Development Cost?

The cost to develop a BNPL app is shaped mainly by feature complexity, KYC verification, credit scoring systems, and payment integrations. Security requirements and the development team’s expertise also play a major role in shaping the final budget.

Q3. How Long Does BNPL Application Development Take?

BNPL application development usually takes 3 to 12 months, depending on project scope. A basic MVP can launch within a few months, while enterprise platforms need additional time for compliance checks, testing, and third-party integrations.

Q4. Is It Better to Launch a BNPL MVP Before Building a Full Platform?

Yes. Launching an MVP first helps validate market demand and collect real user feedback before scaling further. This approach also keeps BNPL MVP development costs lower while reducing the financial risk of building a full-scale platform too early.

Q5. What Technologies Are Commonly Used in BNPL App Development?

Most platforms use React Native or Flutter for the frontend, with Node.js or Python powering the backend. Cloud infrastructure, banking APIs, and security frameworks support API integration for BNPL features and secure payment processing across the platform.

{kind=link}