“Revolutionize the Fintech Industry with new Business tactics and modern technologies.”

The fintech industry is evolving rapidly, driven by technological advancements and shifting consumer demands. In 2026, fintech business models are transforming the financial landscape, making banking, payments, and investments more accessible, efficient, and secure.

From decentralized finance (DeFi) to embedded finance and AI-driven financial services, these fintech startup ideas are reshaping traditional banking. Digital-only neobanks, blockchain-based lending platforms, and pay-as-you-go insurance models are gaining traction. Additionally, green finance solutions and biometric authentication enhance security and sustainability.

Various types of fintech business models not only improve user experience but also promote financial inclusion worldwide. This blog discovers the top 10 most innovative fintech business models in 2026, highlighting how they are evolving the industry.

Market Stats of UAE Fintech Industry

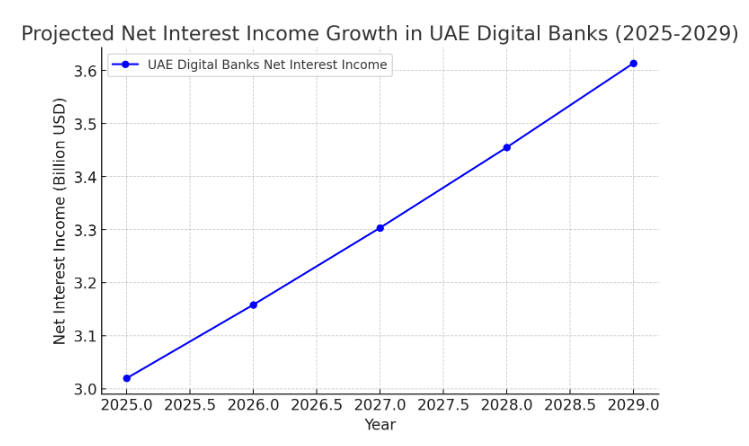

- Net Interest Income is predicted to rise significantly in the United Arab Emirates Digital Banks market, valued at $3.02 Billion by 2026.

- Moreover, it is expected that the Net Interest Income will show a consistent annual growth rate of 59% CAGR between 2025 and 2029, which will result in a market volume of over $3.61 Billion by 2029.

- With an expected value of $528.8 Billion in the year 2026, China is expected to create the greatest Net Interest Income globally.

- Digital banks are becoming more and more popular in the United Arab Emirates as people embrace the accessibility and convenience these tech-driven financial institutions present.

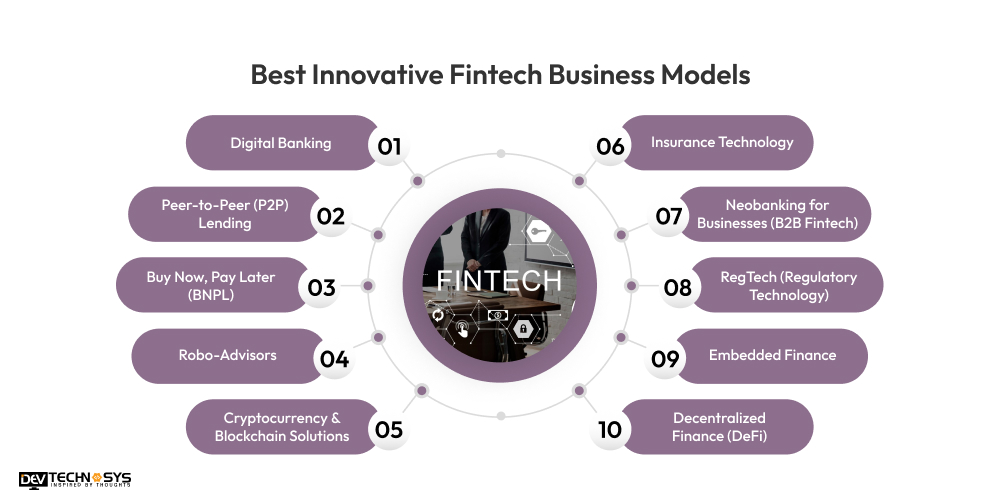

Best Innovative Fintech Business Models

1. Digital Banking

Digital banks run just online, so saving the need for actual offices. They provide services with low fees and improved accessibility including loans, savings accounts, and investments. Digital banks simplify financial management through tailored financial tools and AI-driven automation.

Businesses must know the cost to develop an app like Al Rajhi Bank that delivers fast and easy digital transactions. Additionally, by offering real-time financial data, reduced expenses, and better customer experiences, Chime, Revolut, and Monzo have upended established banking.

Al Rajhi is a digital banking platform by Mashreq Bank, offering a comprehensive suite of banking services through its mobile app, including account management, payments, and investments.

2. Peer-to-Peer (P2P) Lending

By bypassing conventional institutions, P2P lending sites link borrowers directly with investors. These sites use artificial intelligence-driven risk assessment to quickly approve loans at reasonable rates. While investors get more than with traditional savings accounts, borrowers win from reduced interest rates.

By offering a dispersed and open structure, sites like LendingClub and Prosper have transformed lending. You should hire an Android app development company to democratize credit, so loans are more easily available to people and small businesses with few borrowing possibilities.

Beehive is a UAE-based P2P lending platform that connects small and medium-sized enterprises (SMEs) seeking finance with investors, facilitating business growth through accessible funding.

3. Buy Now, Pay Later (BNPL)

With BNPL services, customers may buy anything and pay for it in little or no interest installments. Companies like Klarna, Afterpay, and Affirm have become well-known by merging with e-commerce checkout systems. This is one of the best fintech business models that boosts sales and gives customers financial freedom.

BNPL companies rapidly evaluate creditworthiness by using data analytics, guaranteeing responsible lending. Younger generations find BNPL products convenient and accessible, which helps to change customer behavior all around.

Tabby allows users in the UAE to shop at their favorite stores and split their purchases into interest-free payments, enhancing purchasing power and flexibility.

4. Robo-Advisors

Robo-advisors offer automatic financial planning and investment management tools through algorithms. To build individualized portfolios, companies like Betterment and Wealthfront examine consumer data, risk tolerance, and market patterns. These sites provide cheaper costs than conventional financial advisers, therefore opening a larger audience for investment.

Robo-advisors manage portfolios, maximize tax efficiency, and over time enhance the role of Artificial Intelligence in the financial industry. Millennials and first-time investors seeking low-cost, data-driven financial solutions find the idea especially appealing.

Sarwa is a robo-advisory platform offering automated investment solutions, providing diversified portfolios tailored to individual risk profiles and financial goals.

5. Cryptocurrency & Blockchain Solutions

Fintech companies driven by blockchain offer distributed financial solutions, therefore enhancing security and openness. Businesses such as Binance, Coinbase, and Ethereum support smart contracts, distributed finance (DeFi), and bitcoin trading.

By removing middlemen in transactions, blockchain lowers fraud risks and costs. Blockchain is helping many companies with cross-border payments, tokenized assets, and identity verification. The growing acceptance of these mobile app development solutions like cryptocurrencies and NFTs emphasizes the possibility of distributed financial ecosystems to transform the world economy.

BitOasis is one of the largest cryptocurrency exchanges in the Middle East and North Africa, enabling users to buy, sell, and trade digital assets securely.

6. Insurance Technology

Using big data, blockchain, and artificial intelligence, InsurTech startups simplify insurance offerings. Platforms with fast policy issuing, automated claims processing, and usage-based pricing methods include Lemonade and Root Insurance. InsurTech companies provide individualized and reasonably priced insurance solutions by examining consumer behavior and risk profiles.

The banking software development model advances consumer experience, lowers fraud, and increases openness. As consumers seek digital-first services, InsurTech is turning conventional insurance into a more customer-centric and efficient sector.

Bayzat offers HR and insurance solutions tailored to SMEs in the UAE, providing employee benefits administration, payroll services, and health insurance.

7. Neobanking for Businesses (B2B Fintech)

Unlike digital banks for consumers, neobanks for companies offer specific financial services including automated invoicing, payroll handling, and cash flow projection. Startups and SMEs can get customized payment fintech solutions from companies like Brex and Mercury. These systems maximize financial processes by including artificial intelligence and machine learning, therefore lowering administrative tasks.

B2B neo banking simplifies financial management using seamless connections with accounting software and business tools, therefore facilitating the effective scaling of companies.

Read more: How to Build a Fintech App Like urpay?

NeoBiz by Mashreq Bank is a digital banking service tailored for SMEs, offering business accounts, payments, and cash management solutions through a user-friendly mobile app.

8. RegTech (Regulatory Technology)

Through automation and artificial intelligence, RegTech solutions enable financial firms to follow laws. These tools simplify Know Your Customer (KYC), Anti-Money Laundering (AML), and risk assessment procedures including ComplyAdvantage and Onfido. Financial companies lower expenses, limit human mistakes and improve security by automating compliance chores.

RegTech solutions are crucial for fintech businesses to remain compliant while concentrating on expansion and innovation since rising global regulatory criteria call for them. So, you must contact a banking & finance software development company to manage the demand for fraud detection and digital identity validation.

Monami Tech is a regtech startup providing compliance solutions for financial institutions, helping them navigate AML (anti-money laundering) and KYC (know-your-customer) regulations.

9. Embedded Finance

By including financial services into non-financial platforms, embedded finance lets businesses present payment, loan, or banking options without having to become a financial institution. Two instances are Uber’s driver debit cards and Shopify’s merchant loans. This approach offers flawless financial solutions inside current ecosystems, hence improving client experience.

Through more simple and accessible financial transactions, embedded finance is transforming sectors including e-commerce, logistics, and healthcare. Businesses can hire dedicated mobile app developers to provide value-added financial services that are driving fast expansion of the market.

CredibleX is an embedded finance platform enabling businesses to offer instant lending solutions to their SME customers and suppliers, enhancing access to financing.

10. Decentralized Finance (DeFi)

Through blockchain-based smart contracts, DeFi removes middlemen in financial transactions so users may access lending, borrowing, and trading. Without traditional banks, platforms such as Aave, Uniswap, and MakerDAO let users earn interest, offer liquidity, and participate in automated financial transactions.

So, it is profitable for businesses to build an app like Monzo that enables consumers to take complete control over their assets. DeFi is becoming a potent substitute for centralized financial systems as blockchain acceptance increases, therefore allowing global financial inclusion and innovation.

Jibrel Network is a blockchain-based platform enabling the trading of traditional financial assets using cryptocurrency, pioneering the integration of blockchain technology in the UAE.

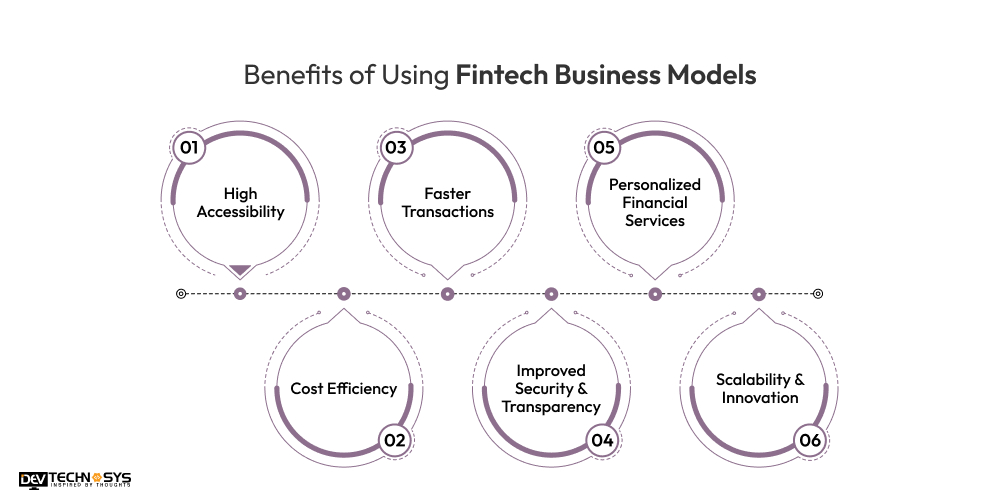

Benefits of Using Fintech Business Models

By providing quicker, more efficient, customer-centric services, fintech business models are changing the banking sector. For companies as well as customers, these models use technology to improve accessibility, security, and economy of cost.

1. High Accessibility

Fintech solutions offer financial services to underbanked and unbanked groups among other more general audiences. A custom web development company could help you to use blockchain technologies, mobile payments, and digital banking to eliminate geographical constraints so customers may access financial. It promotes financial inclusion and enables people to engage in the worldwide economy.

2. Cost Efficiency

Operating expenses and fees abound in traditional banking and financial services. Using blockchain, artificial intelligence, and automation, banking fintech models cut transaction fees, remove middlemen, and expedite procedures. Lower overhead costs help businesses; consumers gain from cheaper fees and improved financial products at reasonable rates.

3. Faster Transactions

Fintech systems speed up transactions through real-time processing technologies. Digital payment options, peer-to-peer transactions, and blockchain-based smart contracts make instant fund transfers and settlements possible. The use of iOS app development services increases efficiency and benefits cross-border transactions by lowering delays and streamlining worldwide financial exchanges.

4. Improved Security & Transparency

Blockchain technology, artificial intelligence-driven fraud detection, and advanced encryption help to increase financial transaction security. Profitable fintech ideas guarantee data integrity, ward against cybercrime, and improve financial processes’ openness. Distributed ledgers and smart contracts will help companies lower fraud risks and build investor and consumer confidence.

5. Personalized Financial Services

Big data analytics and artificial intelligence help fintech startups to provide very customized financial products depending on consumer behavior and preferences. To implement predictive analytics and credit scoring systems you can contact a full stack development company in UAE. By offering pertinent and tailored financial solutions, this personalization increases consumer pleasure and loyalty.

6. Scalability & Innovation

Fintech models are meant to be fast-expanding and flexible. Embedded finance, APIs, and cloud computing let companies effectively scale their offerings. Startups and businesses may react to market needs, fast launch fresh financial products, and remain competitive in the changing financial scene. The constant innovation in fintech guarantees enhancements in customer experience and service offers.

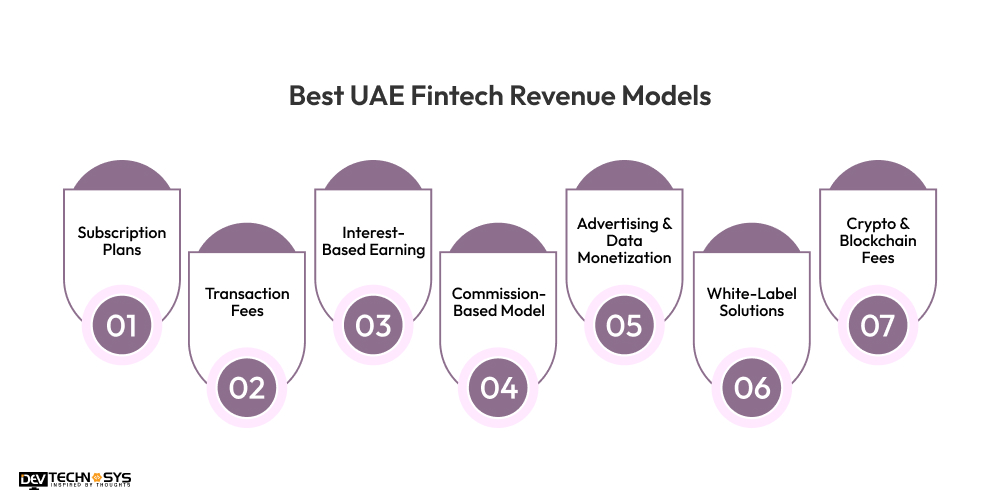

Best UAE Fintech Revenue Models

The UAE fintech industry is changing quickly thanks to several revenue sources allowing startups and financial companies to flourish. These fintech revenue models guarantee profitability and provide creative financial ideas to companies and individuals.

1. Subscription Plans

Many UAE fintech companies use a subscription approach, whereby consumers pay a monthly or annual charge for premium financial services. It is beneficial to hire a mobile app development company that uses tie-red pricing plans with special features including advanced analytics and investing tools abound from digital banks, wealth management platforms, and budgeting applications.

2. Transaction Fees

Charging a nominal percentage of each transaction helps fintech businesses make money. This is followed by digital wallets, remittance services, and payment gateways like PayBy and Telr. For UAE fintech companies’ business models, transaction-based income remains a steady and scalable source of income even with the surge in cashless transactions.

3. Interest-Based Earning

By lending money and collecting interest on repayments, digital lending services create income. Fintech companies with UAE bases such as YAP and Beehive provide credit solutions, SME finance, and peer-to-peer lending. This approach helps to balance the cost to build a banking app in UAE and fintech businesses looking for long-term profitability as well as borrowers wanting flexible lending choices.

4. Commission-Based Model

Certain fintech companies make commissions by collaborating with outside service providers, therefore facilitating transactions. For introducing consumers to wealth management fintech ideas, investment platforms, BNPL services, and insurance aggregators like Souqalmal and Policybazaar UAE pay fees. This approach matches transaction volumes and customer involvement with fintech revenue.

5. Advertising & Data Monetization

Large user base fintech apps employ data analytics and focused advertising to generate income. Offering insights to companies and financial institutions, financial platforms profit from anonymized user data. Businesses should avail of finance software development services to guarantee user privacy compliance while letting fintech ventures create extra cash.

6. White-Label Solutions

Many UAE fintech business opportunities provide banks and financial institutions white-label, or Software-as-a-Service (SaaS) solutions based on their technologies. Without starting from nothing, this methodology helps companies to include fintech technologies including digital banking infrastructure, compliance automation, and AI-driven financial tools into their operations.

7. Crypto & Blockchain Fees

Blockchain technology’s emergence in the United Arab Emirates has helped fintech companies profit from blockchain-based financial services and cryptocurrency transaction fees. A software development company can provide Blockchain-powered payment networks, distributed finance (DeFi) apps, and crypto trading platforms to pay fees for transactions, wallet services, and token exchanges.

Winding Up!!

At last, now it’s time to summarize all the fintech startup business models that we have discussed in this blog. Additionally, we have also seen the impact of these fintech business models on the human life and transformation they have experienced. For businesses it is important to use suitable banking & finance software development services for developing modern solutions.

There are multiple fintech innovation strategies available to guide big and small entrepreneurs through the fintech industry. So, it is important for both investors and people to follow these fintech startup models to get industrial advantage to experience new transformation.

FAQs

1. What are the key trends driving fintech innovation in 2026?

Decentralized finance (DeFi), embedded finance, AI-powered automation, sustainable investing, and open banking are all influencing fintech in 2026. These trends center on employing cutting-edge technology like blockchain and machine learning to streamline transactions, improve financial accessibility, and improve user experiences.

2. How are decentralized finance (DeFi) models evolving in 2026?

DeFi platforms are expanding beyond conventional loan and trade to provide cross-chain interoperability, tokenized assets, and insurance based on smart contracts. DeFi is becoming more popular and enticing to both institutional and retail investors thanks to improved security procedures and regulatory compliance requirements.

3. What is embedded finance, and why is it a game-changer?

Financial services are immediately integrated into non-financial platforms including ride-hailing applications, e-commerce, and healthcare through embedded finance. This strategy makes financial services more comfortable and accessible for consumers by facilitating smooth transactions, rapid insurance, and customized financing alternatives.

4. How is AI revolutionizing fintech business models?

Fintech models powered by AI use machine learning to detect fraud, evaluate credit risk, and create highly customized financial plans. Financial services are becoming more intelligent and user-focused as a result of cost savings and increased efficiency brought about by chatbots, robo-advisors, and AI-powered underwriting procedures.

5. What role does sustainability play in fintech business models?

With firms concentrating on ethical investing, carbon footprint tracking, and digital platforms for green bonds, green finance is growing. Businesses are using blockchain to promote sustainable financial practices through AI-driven insights and transparent ESG (Environmental, Social, and Governance) investing.

{kind=link}