Key Takeaways:

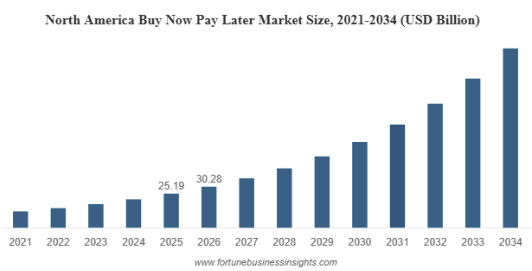

- The global buy now pay later market size is projected to grow from USD 54.56 billion in 2026 to USD 286.02 billion by 2034

- The cost to build an app like Comfi ranges from $30,000 to $150,000, based on project complexity and developer expertise.

- A BNPL app like Comfi requires building a real-time financial infrastructure combining credit underwriting, secure payments, compliance systems, and scalable cloud architecture.

- While thinking of creating a fintech app like Comfi, BNPL startups often focus heavily on rapid user acquisition and smooth checkout experiences.

For businesses and consumers alike, flexible payment solutions have become a key driver of modern commerce. Buy Now Pay Later (BNPL) platforms like Comfi are transforming the lending landscape by enabling customers to make purchases instantly while spreading payments over time. Beyond improving affordability, these platforms help merchants increase sales, boost customer retention, and enhance cash flow.

However, building a successful BNPL app involves much more than integrating payment features; it requires robust credit assessment, fraud prevention, regulatory compliance, and seamless user experiences. In this comprehensive guide to build a buy now pay later app like Comfi, we’ll explore how to build an app like Comfi, covering its features, development process, technology stack, costs, and business considerations.

What is the Comfi App?

This is a B2B (business-to-business) fintech platform designed to streamline cash flow and sales. For Vendors: Allows software (SaaS) and service companies to offer their customers “buy now, pay later” (BNPL) or flexible payment terms (e.g., 30 to 90 days). The vendor gets paid the full amount upfront, while Comfi takes on the collection risk. For Buyers: Enables businesses to split large annual invoices into smaller, manageable chunks without affecting credit scores or paying exorbitant interest.

Buy Now Pay Later Market Stats

- The global buy now pay later market size is projected to grow from USD 54.56 billion in 2026 to USD 286.02 billion by 2034, exhibiting a CAGR of 23% during the forecast period.

- According to UNCTAD, the U.K. saw a spike in online transactions from 15.8% to 23.3%, while China’s rose from 20.7% to 24.9%.

- The U.S. Federal Reserve data reveal that credit card utilization presently stands at approximately 21%.

- The online segment will account for 84.7% market share in 2026.

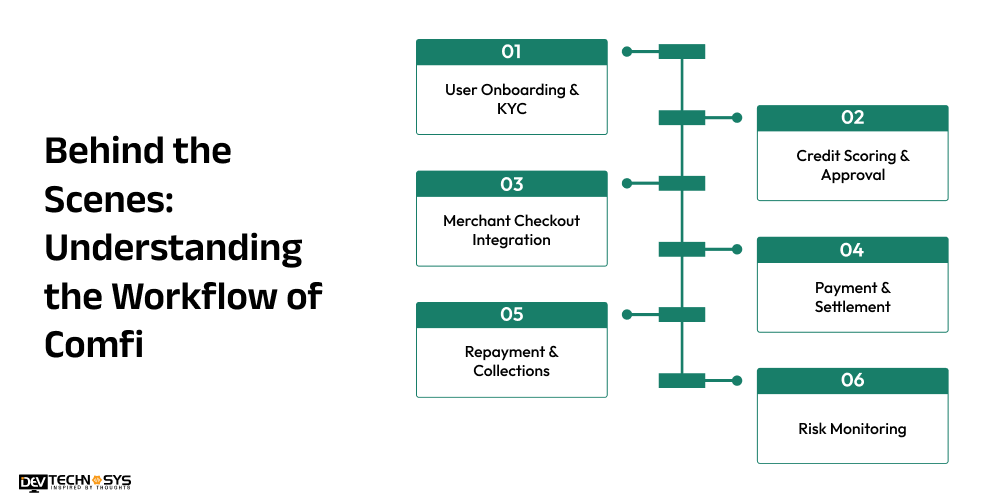

Behind the Scenes: Understanding the Workflow of Comfi

Comfi’s workflow combines real-time credit decisioning, seamless merchant integration, automated repayments, and advanced risk monitoring to deliver a secure and scalable BNPL experience. Before learning how to build a buy now pay later app like Comfi, let’s understand its functionality in detail:

1. User Onboarding & KYC

Users register on the platform and complete KYC verification using identity documents and digital checks, ensuring regulatory compliance and reducing fraud risks at the onboarding stage.

2. Credit Scoring & Approval

An AI-powered credit engine analyzes user behavior, financial history, and alternative data in real time to assign credit limits and approve or reject BNPL requests instantly.

3. Merchant Checkout Integration

At checkout, Comfi’s BNPL API integrates with merchant systems, enabling seamless payment selection and instant credit approval within seconds without disrupting the purchase experience.

4. Payment & Settlement

Once approved, Comfi alternative pays the merchant upfront or on a scheduled cycle, ensuring smooth cash flow while the customer repays the amount in structured installments.

5. Repayment & Collections

A similar app like Comfi automates EMI schedules, reminders, and repayment tracking using payment gateways, SMS, email alerts, and auto-debit systems to improve repayment consistency.

6. Risk Monitoring

Comfi alternative involves continuous fraud detection systems that monitor transactions, user behavior, and repayment patterns in real time to identify anomalies, reduce defaults, and ensure platform security.

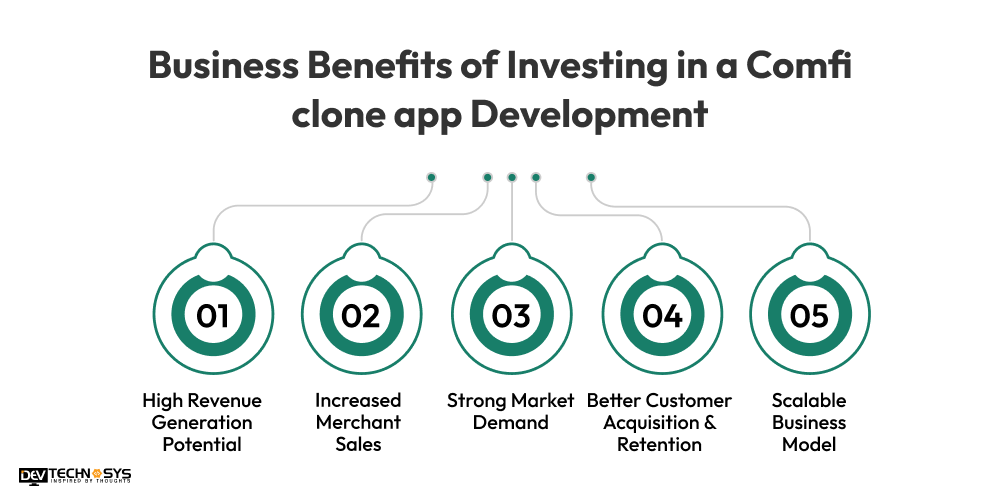

Business Benifits of Investing in a Comfi Clone App Development

The Buy Now Pay Later (BNPL) model is transforming how consumers shop by offering flexible payment options and improving affordability. Investing in a Comfi clone app enables businesses to tap into this fast-growing fintech market with strong revenue potential and scalability.

1. High Revenue Generation Potential

A Comfi-like BNPL app opens multiple income streams such as merchant commissions, interest charges, late fees, and subscription models, ensuring strong and scalable revenue opportunities.

Industry Insights: According to Grand View Research, the global digital payments market is projected to reach $361.3 billion by 2030, growing at a 21.4% CAGR, creating strong opportunities for BNPL-driven revenue models.

2. Increased Merchant Sales

Investing in a BNPL app development solution helps merchants boost conversions by allowing customers to buy products instantly and pay later, leading to higher average order value and improved sales performance.

3. Strong Market Demand

Build a buy now pay later app like Comfi to meet the strong market demand. The Buy Now Pay Later model is rapidly growing across eCommerce and retail sectors, making it a high-demand fintech solution with significant long-term business potential.

4. Better Customer Acquisition & Retention

Businesses should build an app like Cash Advance for better customer acquisition. Flexible payment options attract more users and improve customer loyalty, as consumers prefer platforms that offer affordability and easy installment-based purchasing.

5. Scalable Business Model

A Comfi clone app is highly scalable using cloud infrastructure and API-based integrations, allowing businesses to expand across regions, merchants, and financial products efficiently.

How to Build a Buy Now Pay Later App Like Comfi in Simple Steps?

A BNPL app like Comfi requires building a real-time financial infrastructure combining credit underwriting, secure payments, compliance systems, and scalable cloud architecture. It supports fast, reliable, and risk-controlled lending operations.

1. Market Research & Financial Modeling

Start by analyzing BNPL demand, competitor platforms, and regional lending regulations. Define unit economics such as CAC, LTV, MDR, and expected default rates. This helps design a sustainable business model and identify target segments like B2C, B2B, or embedded finance ecosystems.

Industry Insights: According to Investopedia, the BNPL industry is expected to reach 900 million users worldwide by 2030, underscoring substantial adoption potential.

2. System Architecture & Core Design

Hire a top mobile app development company to design a scalable, microservices-based architecture with independent modules for user management, credit scoring, payments, and collections. To build a buy now pay later app like Comfi, Use API-first development, event-driven messaging (Kafka/RabbitMQ), caching (Redis), and distributed systems to ensure low-latency approvals and high transaction reliability at scale.

3. Technology Stack Selection

If you want to build a buy now pay later app like Comfi, choose a fintech-grade stack including React/Flutter for frontend, Node.js/Java/Go for backend, and PostgreSQL/MongoDB for databases. Deploy on AWS or GCP using Kubernetes for scalability. Implement OAuth 2.0, JWT authentication, and TLS encryption for secure communication and data protection.

| Layer | Technology Options | Purpose / Use |

| Frontend | React.js / Flutter | User interfaces for web and mobile apps |

| Backend | Node.js / Java (Spring Boot) / Go | APIs, business logic, and transaction handling |

| Database | PostgreSQL / MongoDB | Stores user, transaction, and repayment data |

| Cloud Infrastructure | AWS / Google Cloud (GCP) | Hosting, scalability, and system reliability |

| Container Orchestration | Kubernetes | Manages deployment and scaling of services |

| Authentication | OAuth 2.0 / JWT | Secure login and API access control |

| Security | TLS Encryption | Secure data communication and protection |

4. Credit Scoring & Risk Engine

Develop an AI-driven underwriting system using credit bureau data, transaction history, and alternative behavioral signals. According to experts who provide BNPL app development services, machine learning models like XGBoost or logistic regression enable real-time credit decisions in milliseconds. Combine rule-based logic with predictive analytics for accurate risk assessment.

5. Payment Gateway & Banking Integration

To build a BNPL app like Comfi, integrate secure payment gateways and banking APIs for instant merchant settlements and EMI processing. Support auto-debit via cards, UPI, or ACH. Use tokenization to secure sensitive data and reduce PCI compliance scope while ensuring smooth repayment and transaction flows.

6. Merchant & Customer Applications

Build dual interfaces for an app like Madfu: a customer app for checkout, credit tracking, and repayments, and a merchant portal for onboarding, invoicing, and analytics. To make a buy now pay later app like Comfi, use real-time WebSockets for updates and optimize UI performance using SSR and lightweight frontend frameworks.

7. Compliance, Security & Fraud Prevention

Implement KYC/AML verification using identity APIs and ensure PCI-DSS compliance for payment security. Add fraud detection layers, including device fingerprinting, behavioral analytics, and anomaly detection models, to prevent identity theft, account takeover, and transactional fraud.

8. Testing, Deployment & Scalability

Hire mobile app developers in Middle East who would perform unit, integration, load, and security testing to ensure security and smooth performance. They use tools like JMeter and OWASP ZAP. Deploy using CI/CD pipelines and containerized infrastructure. Enable auto-scaling and load balancing to handle high transaction volumes during peak usage periods.

10 Advanced Features of a BNPL App Like Comfi

BNPL apps like Comfi are powered by advanced fintech systems that combine instant credit decisioning, secure payments, and intelligent risk management. These features, to build a buy now pay later app like Comfi, ensure a seamless and scalable lending experience.

| User Panel | Admin Panel | Merchant/System Panel |

| Instant Credit Approval | Risk Management System | Merchant Onboarding & KYB Verification |

| Smart EMI Management | Fraud Detection Engine | API & Payment Integration Layer |

| One-Tap BNPL Checkout | User & Merchant Management | Payment Orchestration System |

| Credit & Spending Dashboard | Financial Analytics Dashboard | Real-Time Transaction Monitoring |

| Repayment Reminders & Alerts | Credit Scoring Engine Control | Automated Settlement System |

| Auto-Debit Payment Option | Dispute & Chargeback Management | Invoice Management System |

| Credit Limit Management | Compliance & Regulatory Monitoring | Multi-Gateway Payment Support |

| Transaction History Tracking | Portfolio Risk Analysis | Banking API Connectivity |

| Reward & Loyalty Program | AI Decision Engine Controls | Merchant Revenue Dashboard |

| Support & Help Center | Audit & Reporting System | Fraud Monitoring Layer |

1. AI-Based Credit Scoring Engine

A fintech app development company creates a Comfi clone app by using machine learning algorithms and alternative data sources like behavior, transactions, and credit bureau data to assess risk and approve credit instantly in real time.

2. Dynamic Credit Limit System

Continuously updates user credit limits based on repayment history, spending patterns, income signals, and risk profiling to ensure responsible lending and reduce default risk exposure.

3. Instant BNPL Checkout Integration

This feature is crucial to build a buy now pay later app like Comfi. It enables a seamless one-click checkout experience by embedding BNPL options directly into merchant platforms, ensuring fast approval and frictionless purchase completion for customers.

4. Smart EMI Scheduling System

Make a buy now pay later app like Comfi that automatically generates flexible installment plans based on transaction value, tenure selection, and user risk profile, ensuring affordability and improving repayment consistency across users.

5. Real-Time Fraud Detection

Uses advanced behavioral analytics, device fingerprinting, and AI-based anomaly detection models to identify suspicious activities and prevent fraudulent transactions instantly during payment processing.

6. Automated Collections Engine

Manages repayment cycles using smart reminders, SMS/email notifications, auto-debit systems, and escalation workflows to reduce delays and improve overall repayment efficiency significantly.

7. Merchant Settlement System (T+0/T+1)

To create a buy now pay later app like Comfi ensures fast merchant payouts through integrated banking APIs and payment gateways, improving cash flow and enabling instant or next-day settlement processing for businesses.

8. Multi-Gateway Payment Integration

Create a buy now pay later app like Comfi that supports multiple payment channels, including cards, UPI, wallets, ACH, and banking APIs, to ensure high transaction success rates and an uninterrupted payment processing experience.

9. Advanced Analytics Dashboard

Build a BNPL App Like Sympl that provides real-time insights into credit performance, repayment behavior, default rates, and revenue metrics, helping businesses make data-driven decisions and optimize financial operations effectively.

10. Open API & Embedded Finance Layer

Enables seamless integration with eCommerce platforms, fintech apps, and third-party systems using secure APIs, supporting scalable embedded finance and ecosystem expansion.

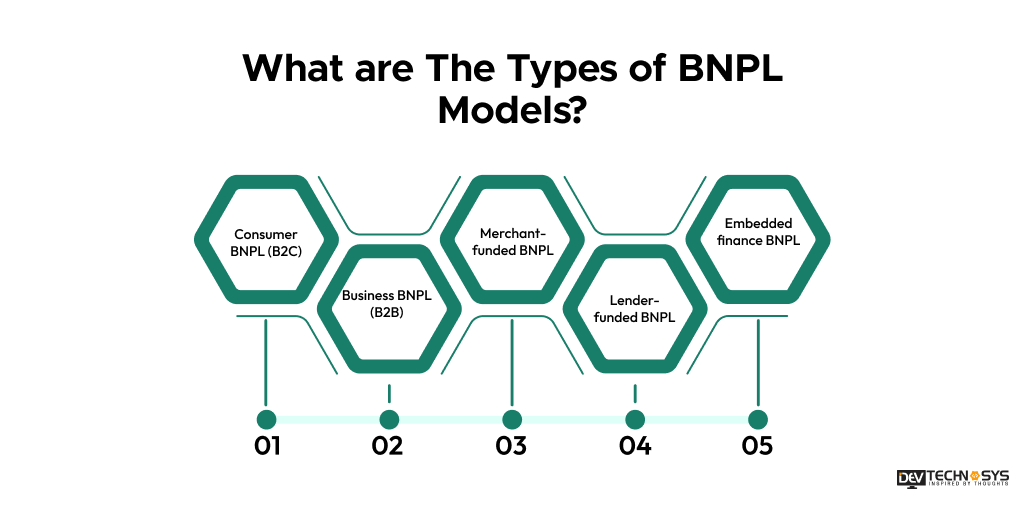

What are The Types of BNPL Models?

The BNPL ecosystem operates through multiple financing structures that define who funds the credit, who manages the risk, and how repayments are handled. The different types of BNPL models are:

1. Consumer BNPL (B2C)

This model allows individual customers to purchase products and services instantly and pay later in installments. It is widely used in eCommerce, retail, travel, and digital shopping platforms to improve affordability and conversion rates.

2. Business BNPL (B2B)

B2B BNPL enables businesses to buy goods or services on credit and repay later. Buy Now Pay Later app development for the B2B model helps SMEs manage cash flow, improve procurement flexibility, and access short-term financing without traditional loan processes.

3. Merchant-Funded BNPL

In this model, merchants bear the financing cost by paying fees to BNPL providers. In return, they benefit from increased sales, higher order values, and improved customer retention.

Industry Insights: According to Bain, BNPL significantly improves purchasing behavior. Studies show 57% of merchants reported higher basket conversion, while 46% experienced increased average order value (AOV) after offering BNPL payment options.

4. Lender-Funded BNPL

Here, banks or financial institutions provide the capital for transactions. BNPL providers act as intermediaries, managing credit assessment, repayment collection, and risk management while lenders fund the purchases.

5. Embedded Finance BNPL

Android app development experts create this model by integrating BNPL services directly into third-party platforms via APIs. It enables seamless checkout experiences inside apps like eCommerce, SaaS platforms, or fintech ecosystems without redirecting users externally.

Top 5 Comfi Alternatives to Explore in 2026?

The BNPL ecosystem is rapidly evolving, offering businesses flexible financing solutions that improve cash flow, boost conversions, and enhance customer experience. Platforms like PayPal, GoCardless, Sunbit, Sezzle, and Klarna are emerging as strong alternatives to Comfi for B2B payment needs.

1. PayPal Payments

PayPal is a globally trusted BNPL and payment solution offering Pay in 4, invoicing, and secure checkout. It supports both B2B and B2C transactions, improving trust, reducing friction, and enabling fast international payment processing. If you want to build a similar app like PayPal, contact a reputable eWallet app development company

2. GoCardless

GoCardless specializes in automated recurring payments through direct debit systems. Buy Now Pay Later app development experts make it for subscription and B2B businesses, helping reduce failed payments, automate collections, and improve predictable cash flow management across global markets.

3. Sunbit

Sunbit offers fast point-of-sale financing with high approval rates and quick decisions. It uses alternative credit models, making it suitable for businesses handling larger purchases while reducing dependency on traditional credit bureau systems.

4. Sezzle

Sezzle provides flexible, interest-free installment payments that integrate easily with eCommerce platforms like Shopify. It improves conversion rates by allowing customers to split payments into manageable, short-term installments without hidden charges.

5. Klarna

Klarna offers flexible BNPL options such as Pay in 30 Days and monthly financing plans. It enhances customer affordability, increases purchase conversions, and helps businesses maintain smoother cash flow with delayed payment structures.

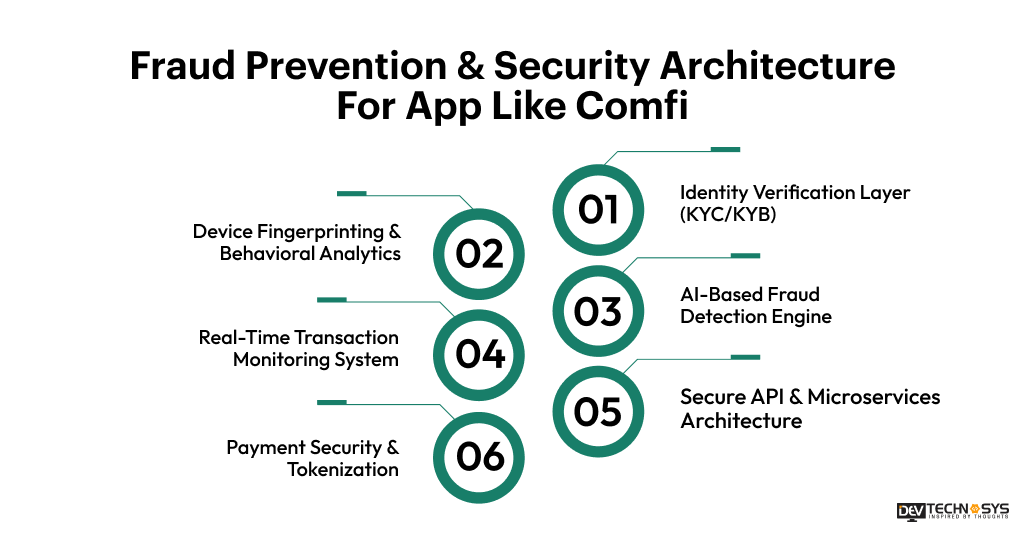

Fraud Prevention & Security Architecture For App Like Comfi

Building a BNPL app like Comfi requires a strong, layered security architecture because it handles sensitive financial data, credit risk, and real-time transactions. Fraud prevention must be embedded at every stage of the user journey, from onboarding to repayment.

1. Identity Verification Layer (KYC/KYB)

The first defense layer required to develop a Buy Now Pay Later app like Comfi is identity verification. It ensures only legitimate users and merchants enter the system. It uses KYC (Know Your Customer) and KYB (Know Your Business) verification through document validation, biometric checks, liveness detection, and government database verification APIs like Onfido or Jumio.

2. Device Fingerprinting & Behavioral Analytics

Each user device is uniquely identified using device fingerprinting techniques such as IP tracking, browser metadata, and OS signals. Combined with behavioral analytics (typing speed, navigation patterns), the system detects anomalies that indicate fraud or account takeover attempts.

3. AI-Based Fraud Detection Engine

Machine learning models continuously analyze transaction patterns in real time. Algorithms like random forest, gradient boosting, and anomaly detection models flag unusual behavior such as rapid purchases, unusual locations, or high-risk spending patterns.

4. Real-Time Transaction Monitoring System

Every transaction passes through a risk scoring engine before approval. If risk thresholds are exceeded, the system can decline, hold, or route transactions for manual review. This ensures instant fraud prevention without affecting legitimate users.

5. Secure API & Microservices Architecture

When you develop a buy now pay later app like Comfi, remember that it relies on API-first microservices architecture secured with OAuth 2.0, JWT tokens, TLS encryption, and rate limiting. This prevents unauthorized access, API abuse, and data breaches across distributed services.

6. Payment Security & Tokenization

Sensitive payment data is never stored directly. Instead, tokenization replaces card or bank details with secure tokens. This reduces PCI-DSS compliance risk and protects users from data leaks and interception attacks.

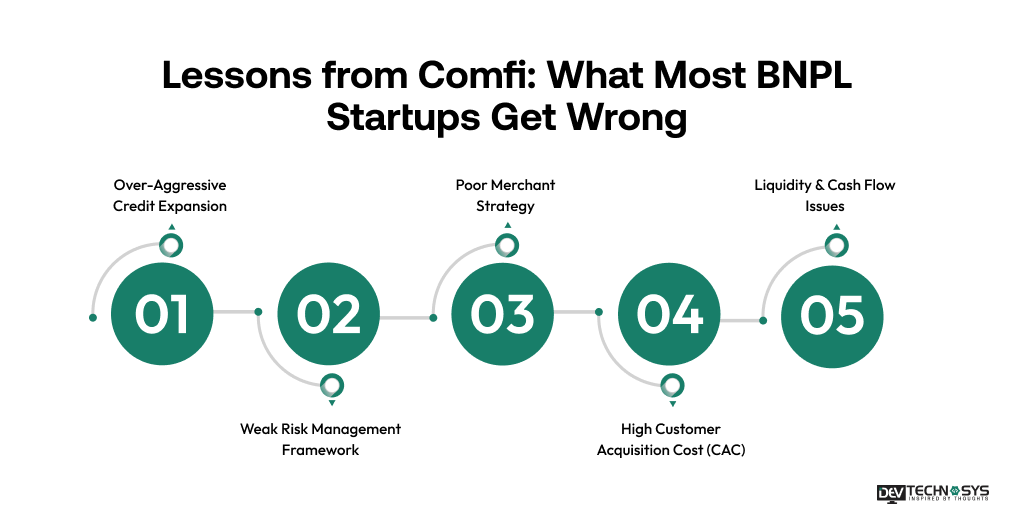

Lessons from Comfi: What Most BNPL Startups Get Wrong

BNPL startups often focus heavily on rapid user acquisition and smooth checkout experiences, but overlook the financial and operational complexity behind sustainable lending. Platforms like Comfi highlight the importance of balancing growth with risk control, compliance, and long-term profitability.

1. Over-Aggressive Credit Expansion

Many startups approve too many users too quickly without strong underwriting systems. Weak credit scoring models lead to higher default rates and unstable portfolio health, especially in early-stage scaling.

2. Weak Risk Management Framework

Startups often underestimate fraud, chargebacks, and repayment defaults. Without AI-driven risk engines, device intelligence, and real-time monitoring, financial exposure increases significantly.

3. Poor Merchant Strategy

If the experts who build the best instant loan applications in UAE focus only on users while ignoring merchant onboarding, it creates an imbalance. Successful BNPL platforms prioritize merchant incentives, seamless integration, and fast settlement cycles.

4. High Customer Acquisition Cost (CAC)

Many BNPL companies overspend on marketing without optimizing lifetime value (LTV). Sustainable models rely more on partnerships, referrals, and embedded finance integrations.

5. Liquidity & Cash Flow Issues

An iOS app development company creates BNPL with strong capital backing since merchants are paid up front. Poor treasury planning leads to liquidity gaps, especially when repayment cycles are delayed or default rates rise.

Key Insight: The biggest mistake BNPL startups make is treating it as a payment app rather than a credit infrastructure business. Success depends on strong underwriting, risk controls, a balanced merchant ecosystem, and disciplined financial management.

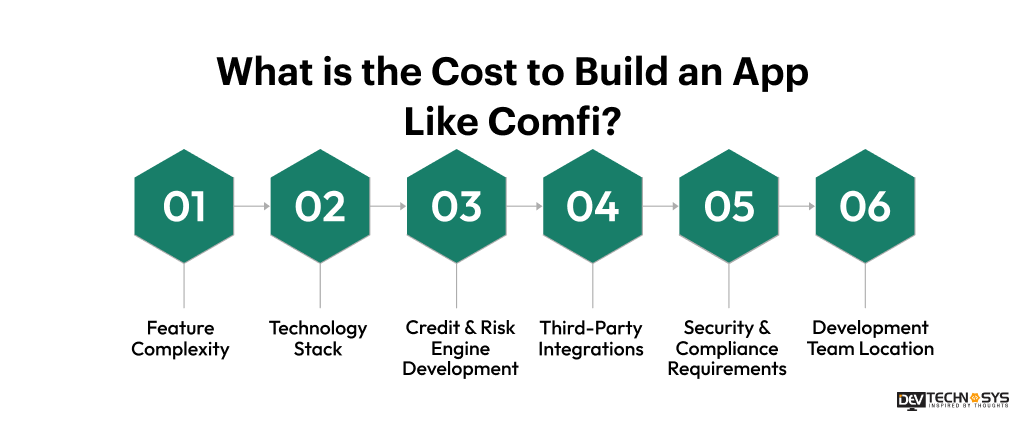

What is the Cost to Build an App Like Comfi?

The cost to build an app like Comfi is around $30,000 to $150,000. The cost changes significantly due to features, platform, UI/UX design, third-party integrations, developers’ location, and more. The basic BNPL mobile app development cost is between $30,000 to $60,000. The cost to develop an app like Comfi for a mid-level app is between $60,000 to $100,000. The cost to build an app like Comfi with advanced features and functionality is $100,000 to $150,000.

1. Feature Complexity

The overall cost to develop a buy now pay later app like Comfi increases with advanced features like AI credit scoring, EMI management, fraud detection, and real-time approvals, as each module requires complex logic, backend systems, and integration-heavy development efforts.

2. Credit & Risk Engine Development

Building a smart underwriting system using credit bureau APIs, alternative data sources, and machine learning models increases the cost to build an app like Comfi significantly. It requires real-time decisioning, data engineering, model training, and continuous optimization for accurate risk assessment and fraud prevention.

3. Third-Party Integrations

Integrating payment gateways, banking APIs, KYC providers, credit bureaus, and fraud detection tools increases development complexity and mobile app maintenance cost. Each integration requires secure API architecture, compliance validation, testing cycles, and ongoing maintenance for seamless financial operations.

4. Security & Compliance Requirements

Compliance with PCI-DSS, GDPR, AML, and KYC regulations increases the cost to build an app like Comfi due to encryption systems, audits, legal approvals, and continuous monitoring. A strong security architecture is essential for protecting sensitive financial data and ensuring regulatory compliance.

5. Development Team Location

Development cost varies based on geography and expertise. If you hire dedicated developer from US and Europe, the hourly charges will be higher, while Asia-based developers offer cost-effective solutions with strong fintech experience, enabling businesses to balance budget and quality effectively.

6. Maintenance & Support Services

Post-launch maintenance includes bug fixes, security patches, API updates, performance optimization, and server monitoring. Continuous updates are essential for uptime, compliance, and smooth user experience, adding to the cost to build a buy now pay later app like Comfi.

| Factor | Estimated Cost Contribution |

| Feature Complexity | $5,000 – $40,000 |

| Technology Stack | $3,000 – $20,000 |

| Credit & Risk Engine Development | $8,000 – $35,000 |

| Post-launch maintenance | $5,000 – $8,000 |

| Security & Compliance Requirements | $4,000 – $20,000 |

| Development Team Location | $5,000 – $30,000 |

How Long Does It Take to Build an App Like Comfi?

Building a BNPL app like Comfi typically takes 3 to 9+ months, depending on feature complexity, integrations, compliance requirements, and team expertise. Simple MVP versions can be launched faster, while enterprise-grade platforms with AI credit scoring, fraud detection, and multi-gateway payment systems require longer development cycles. The timeline is usually divided into structured phases to ensure proper planning, development, testing, and deployment.

| Phase | Duration | Key Activities |

| Discovery & Planning | 2 to 4 weeks | Market research, business model definition, technical architecture, compliance planning |

| UI/UX Design | 3 to 6 weeks | Wireframes, prototypes, and user flows for customer, merchant, and admin panels |

| Core Development | 10 to 16 weeks | Backend, frontend, APIs, credit engine, payment workflows, cloud setup |

| Integrations | 3 to 6 weeks | Payment gateways, banking APIs, KYC, credit bureaus, fraud tools |

| Testing & QA | 3 to 5 weeks | Functional, security, load testing, and compliance validation |

| Deployment | 2 to 3 weeks | Cloud deployment, CI/CD setup, monitoring, and production launch |

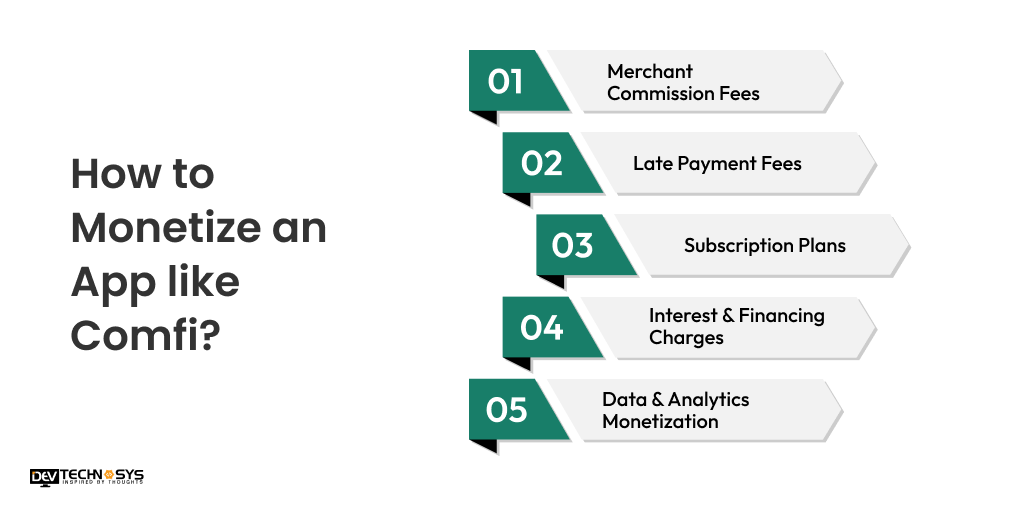

How to Monetize an App like Comfi?

Monetizing a BNPL app like Comfi requires a balanced revenue model that combines transaction fees, financial services, and ecosystem-based earnings. Since BNPL platforms act as intermediaries between merchants, users, and lenders, multiple revenue streams can be built into the system.

1. Merchant Commission Fees

BNPL platforms charge merchants a percentage fee on every transaction processed through the app. This is the primary revenue stream, as merchants benefit from higher conversions and increased order values.

2. Interest & Financing Charges

While short-term BNPL plans are often interest-free, longer repayment durations or high-risk users may incur interest or financing charges. These fees vary based on credit profile, loan tenure, and overall risk assessment of the borrower.

3. Late Payment Fees

BNPL platforms generate revenue through late payment penalties when users miss due dates. These fees also act as a behavioral control mechanism, encouraging timely repayments and reducing default risk across the lending ecosystem.

4. Subscription Plans

Subscription-based monetization offers premium features for users and merchants, such as higher credit limits, reduced transaction fees, faster settlements, and advanced analytics tools, improving overall platform engagement and recurring revenue stability.

5. Data & Analytics Monetization

Aggregated and anonymized financial data is used to generate actionable insights for merchants and lenders. These insights help improve customer targeting, credit risk evaluation, and overall business decision-making strategies.

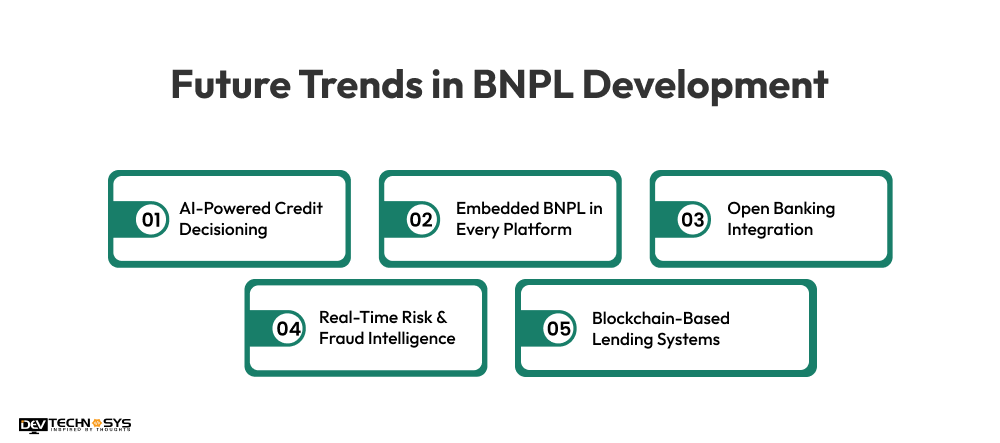

Future Trends in BNPL Development

The BNPL industry is evolving rapidly as fintech companies move beyond simple installment payments toward smarter, AI-driven financial ecosystems. Future BNPL platforms will focus more on automation, embedded finance, and real-time risk intelligence to improve scalability and reduce default rates.

1. AI-Powered Credit Decisioning

Future BNPL systems will rely heavily on advanced AI models that analyze real-time behavioral, transactional, and alternative data to make instant and highly accurate credit decisions with lower default risk.

2. Embedded BNPL in Every Platform

BNPL will become a default payment option embedded directly into eCommerce, SaaS, travel, and even B2B procurement systems through APIs, eliminating the need for standalone BNPL apps.

3. Open Banking Integration

With open banking APIs, BNPL platforms will access real-time bank data to assess income, spending behavior, and financial health, enabling more precise underwriting and dynamic credit limits.

4. Real-Time Risk & Fraud Intelligence

Next-gen BNPL systems will use AI-driven fraud detection, behavioral biometrics, and continuous transaction monitoring to identify and prevent fraud instantly during payment processing.

5. Blockchain-Based Lending Systems

Blockchain will improve transparency in lending by enabling smart contracts for repayments, reducing disputes, and automating settlement processes between users, merchants, and lenders.

Conclusion

Building a Buy Now Pay Later (BNPL) app like Comfi goes beyond split payments; it’s a complete digital lending ecosystem. It requires AI-based credit scoring, secure payment systems, real-time risk management, and strong regulatory compliance. When built well, it boosts merchant sales, improves customer affordability, and creates multiple revenue streams. Success depends on balancing growth, responsible lending, fraud prevention, and scalable architecture.

If you are a business looking for a top BNPL app development company, contact Dev Technosys. We have 15+ years of expertise in creating advanced BNPL apps that help businesses scale.

FAQs

- How Much Does it Cost to Develop an App Like Comfi?

BNPL app development typically costs between $30,000 and $150,000. The total cost to make an app like Comfi depends on AI features, payment integrations, compliance requirements, scalability, and overall platform complexity.

- What Features Are Essential In a BNPL App?

Key features of pay later app development include user onboarding, KYC verification, AI credit scoring, EMI management, merchant dashboard, fraud detection, payment gateway integration, transaction tracking, and analytics reporting systems.

- Is Credit Scoring Necessary For BNPL Apps?

Yes, credit scoring is essential for BNPL mobile app development. It evaluates user eligibility, reduces default risk, and ensures responsible lending decisions using AI models, credit bureau data, and alternative financial behavior signals.

- How Do BNPL Apps Make Money?

They generate revenue through merchant fees, interest charges, late payment penalties, subscription plans, and API monetization via embedded finance partnerships with third-party platforms.

- How Do BNPL Apps Manage Fraud And Risk?

Digital lending app development company uses AI-based fraud detection, device fingerprinting, behavioral analytics, KYC/AML checks, and real-time transaction monitoring to detect and prevent suspicious or high-risk activities.

- Can BNPL Apps Scale Globally?

Yes, with cloud-native infrastructure, multi-currency support, localized compliance, and API-driven architecture, BNPL apps can scale efficiently across multiple international markets.

{kind=link}